Provision Newsletter

8 essential Australian experiences you might not know about

Torndirrup National Park near Albany, WA is astounding.

Credit: Tourism Western Australia

In the words of Captain Obvious, Australia provides some amazing experiences.

What the captain fails to mention, though, is that this wealth of remarkable attractions means some truly incredible experiences are often overlooked.

We thought it was high time to change that, so we put together this superb line-up of underrated Australian activities.

From

Read More

Torndirrup National Park near Albany, WA is astounding.

Credit: Tourism Western Australia

In the words of Captain Obvious, Australia provides some amazing experiences.

What the captain fails to mention, though, is that this wealth of remarkable attractions means some truly incredible experiences are often overlooked.

We thought it was high time to change that, so we put together this superb line-up of underrated Australian activities.

From the easily reached and the inexpensive to the once in a lifetime, exciting adventures await.

Impressive: Umpherston Sinkhole, Mt Gambier, SA.

Credit: SATC/Adam Bruzzone

Exploring Torndirrup National Park, Albany, WA

Sure, Australia teems with treasure-rich national parks that all jostle for attention, but Torndirrup clearly deserves far more footprints than it receives.

It’s massively mesmering: rugged and windswept and crammed with eye-popping, funky features. Among the most impressive is The Gap where the full force of the ocean’s wild fury is laid bare in dramatic fashion. And it’s all easily admired from a raised viewing platform.

Book now: BIG4 Emu Beach Holiday Park or BIG4 Middleton Beach Holiday Park.

The Gap reveals the ocean’s full fury, which not even this picture adequately demonstrates.

Credit: Tourism Western Australia

Climbing the Shot Tower, Hobart, TAS

Found 10km south of the CBD, the Shot Tower was once tasked with manufacturing ammunition. Today, it’s in the firing line of visitors seeking spectacular panoramic vistas.

The structure has a few quirks that enhance the interest, including a sign that proclaims it took eight months to build when the actual figure is more like eight years. Its height is another point of contention.

Book now: BIG4 Hobart Airport Tourist Park.

Fake news? The sign heralding the eight-month completion of the Shot Tower.

Credit: Tourism Tasmania/Kathryn Leahy

Wandering around Umpherston Sinkhole, Mt Gambier, SA

Nature has moulded a wonderful creation, with a little help from humanity. In a former life the sinkhole was a limestone cave before relentless corrosion from seawater resulted in its roof collapsing.

It has since become a spectacular sunken garden with a size and scale that is only truly appreciated with a first-hand visit. Better yet, it’s centrally located and open day and night.

Book now: BIG4 Blue Lake Holiday Park.

Sinking feeling: descend into the depths of Umpherston Sinkhole to appreciate its mammoth size and scale.

An airboat tour of Mary River wetlands, NT

Spotted on the fringes of Kakadu National Park, the wetlands of Mary River are home to a feast of fascinating flora and fauna, including crocs. And witnessing it all while on an airboat is unbeatable.

It’s an exhilarating experience that provides unparalleled access to a mind-blowing section of the Top End. If you’re lucky, your friendly guide will be armed with intimate knowledge of these action-packed surrounds.

Book now: BIG4 Howard Springs Holiday Park.

Strap in for a thrilling ride aboard an airboat.

Swimming at Blue Pool, Bermagui, NSW

Move over Bondi Beach’s Iceberg Pool; Bermagui’s Blue Pool is every bit as alluring. Found in the South Coast NSW region, this natural pool (well, sort of natural) is a prized place for a refreshing swim.

The backdrop of craggy, towering cliffs only adds to the occasion, while the sparkling coastal views afforded from this vantage point are worth a visit alone. Best of all, this experience won’t cost you a cent.

Book now: BIG4 Wallaga Lake Holiday Park.

Blue Pool is a gem of the South Coast NSW region.

Credit: Destination NSW

Delving into the SS Yongala wreck, Ayr, QLD

Admittedly, this site earns much attention – thousands head underwater each year for a diving experience regarded as one of Australia’s best. Yet how many of us can honestly say we know the doomed ship’s backstory? It’s not exactly Titanic like, but details of how the SS Yongala ended up on the sea floor are thoroughly captivating.

Dive tours depart from Ayr and provide an eerie, incredible experience where you’ll be joined by a wealth of magical marine life. Or relive the fascinating yarn at the Townsville Maritime Museum.

Book now: BIG4 Ayr Silver Link Caravan Village or BIG4 Townsville Woodlands Holiday Park.

The backstory of SS Yongala is captivating.

Credit: Yongala Dive

Wander around historical Clunes, Goldfields region, VIC

Although this isn’t the only place in Australia that could claim to be forgotten by time, it certainly seems to be overlooked by the masses. A wander along this old gold-mining town’s main street is like a trip down memory lane – ignore the modern cars – with a streetscape that appears untouched since its creation.

In fact, Clunes is regarded as having the finest collection of 19th century buildings anywhere in Australia, which helps to easily evoke thoughts that you’ve travelled back a century or so. Charming.

Book now: BIG4 parks in the Goldfields region.

Clunes generally only bustles like this for its annual Booktown Festival, held in May.

Touring Coober Pedy, SA

The opal-mining town is hardly a spotlight avoider, but you get the feeling its unique nature warrants more attention. Simply put, Coober Pedy is absolutely mesmerising and a destination that every Australian should experience at least once.

It’s well-known that much of its infrastructure has been built underground so locals can avoid the heat, and it makes for a super interesting and incomparable visit from the moment you enter town. The incredible landscapes in and around Coober Pedy only add to an extremely memorable experience.

Book now: BIG4 Stuart Range Outback Resort.

The landscapes in and around Coober Pedy are jaw-dropping.

Source : BIG4 Holiday Park November 2018

Reproduced with the permission of BIG4 Holiday Parks. This article first appeared on BIG4.com.au and was republished with permission.

Important:

Any information provided by the author detailed above is separate and external to our business and our Licensee. Neither our business, nor our Licensee take any responsibility for any action or any service provided by the author.

Any links have been provided with permission for information purposes only and will take you to external websites, which are not connected to our company in any way. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page.

Retiree self-protection: A volatility-and-downturn ‘bucket’

The latest fall in share prices close to the 10-year anniversary of the global financial crisis (GFC) is likely to prompt more retirees and near-retirees to think about creating a volatility-and-downturn cash bucket.

This is a straightforward strategy intended to reduce the possibility of retirees – particularly those with many years of retirement ahead – having to sell investments at depressed

Read MoreThe latest fall in share prices close to the 10-year anniversary of the global financial crisis (GFC) is likely to prompt more retirees and near-retirees to think about creating a volatility-and-downturn cash bucket.

This is a straightforward strategy intended to reduce the possibility of retirees – particularly those with many years of retirement ahead – having to sell investments at depressed prices to maintain their income in the event of an extended future downturn .

What is a volatility-and-downturn cash bucket?

Retirees and investors approaching retirement often set aside about two to three years of living expenses if possible in a volatility-and-downturn cash bucket. This provides a buffer against being forced to sell assets at the wrong time, which may cut the expected longevity of a portfolio and its ability to produce enough future growth.

In a recent commentary, actuaries Rice Warner emphasises how disciplined investor behaviour is critical to handling a sharp fall in share prices and how a cash bucket can assist them to remain disciplined.

There is typically a close link to market behaviour and investor behaviour. (Regular Smart Investing readers may have read our past discussions of these buckets.)

“The behaviour of stock markets is unpredictable as sentiment big part in short-term price movements,” Rice Warner comments. “When people are upbeat about the economy, prices often rise exuberantly; when the market turns down significantly, it is usually fast and without notice.

“So, while we can say that investment markets,” Rice Warner adds, “follow a cyclical pattern, no one can predict when the market will rise or fall. We also know that markets usually recover their losses over time, sometimes quite quickly.”

And as the commentary says, the impact of a market downturn could be magnified for investors who “lock in losses by moving into more defensive strategies [such as switching to all-cash portfolios] at an inopportune time”.

When and how can I create a cash bucket?

Investors often begin to build-up a cash bucket or buffer in their last few years before their planned retirement. For instance, some investors direct a proportion of their super contributions from their last few years in the workforce into a cash bucket within their super funds.

Other opportunities may arise to create a cash bucket including, say, an inheritance or the sale of an investment property. Some investors will simply increase the asset allocation to cash in their super funds – perhaps when periodically rebalancing their portfolios.

How big should I make my cash bucket?

While investors often set aside two to three years of living expenses in their volatility-and-downturn bucket, the size of the buffer and how it is built-up will depend on such personal circumstances as the size of an individual’s retirement savings, age, investment timeframe and perhaps professional advice. When determining the size of your cash bucket, keep the age pension in mind if applicable.

How can I top-up my cash bucket?

Some investors direct a proportion of unspent income from their main diversified portfolio, such as a balanced or growth super fund, to top-up their cash bucket from time to time – particularly during stronger-performing years. And proceeds from regular rebalancing of an investor’s main diversified portfolio can provide top-up money.

Please contact us on |PHONE| if you would like to discuss.

Source : Vanguard October 2018

Reproduced with permission of Vanguard Investments Australia Ltd

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) is the product issuer. We have not taken yours and your clients’ circumstances into account when preparing this material so it may not be applicable to the particular situation you are considering. You should consider your circumstances and our Product Disclosure Statement (PDS) or Prospectus before making any investment decision. You can access our PDS or Prospectus online or by calling us. This material was prepared in good faith and we accept no liability for any errors or omissions. Past performance is not an indication of future performance.

© 2018 Vanguard Investments Australia Ltd. All rights reserved.

Important:

Any information provided by the author detailed above is separate and external to our business and our Licensee. Neither our business, nor our Licensee take any responsibility for any action or any service provided by the author.

Any links have been provided with permission for information purposes only and will take you to external websites, which are not connected to our company in any way. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page

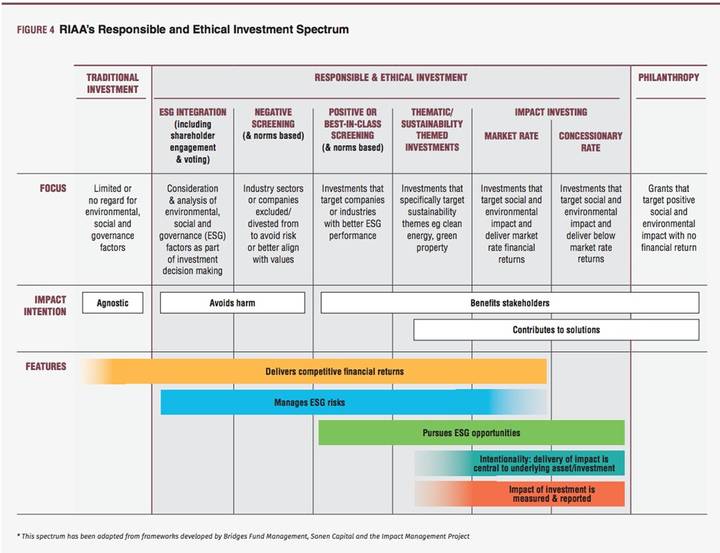

Making an impact or ticking a box

The ongoing growth in environmental, social and governance (ESG) investing has been driven by investors who may share certain common characteristics, but who have different concerns and commitment levels towards ethical investing.

This growth has unsurprisingly been accompanied by a proliferation of ESG product offerings from an increasing number of fund managers. However,

Read More“How well aligned are ESG managers and ESG investors?”

The ongoing growth in environmental, social and governance (ESG) investing has been driven by investors who may share certain common characteristics, but who have different concerns and commitment levels towards ethical investing.

This growth has unsurprisingly been accompanied by a proliferation of ESG product offerings from an increasing number of fund managers. However, they may take significantly different approaches in balancing the need for market performance alongside delivering positive and sustainable social and environmental outcomes.

Investors should recognise that not all ESG managers are created equal. Investors who genuinely wish their savings to be invested within a values-driven framework should identify a manager whose values align with their own, rather than one who merely acknowledges ESG risk management as a hygiene factor.

Sensitivity to performance

ESG investor behaviour is characterised by a sliding scale of commitment amongst investors and consequently the level of priority that they accord it differs.

At one end of the scale are investors who are sometimes described as philanthropic investors and are highly committed to allocating funds within a clearly defined ethical framework. They prioritise making a positive impact ahead of making portfolio returns, especially in the shorter-term.

Further along the scale, many institutions remain focussed on delivering long-term performance to their underlying investors but genuinely take ESG oversight seriously. They may well engage with the fund manager every quarter and pay close attention to the ESG credentials of all stocks within the portfolio.

At the other end of the ESG commitment scale are investors for whom ESG is perceived as a hygiene factor while their primary focus is firmly on maximising returns. The expectation is that controls are in place to manage the most significant ESG risks and ensure that the governance requirements of the mandate are being met.

Source: Responsible Investment Association Australasia – https://responsibleinvestment.org/wp-content/uploads/2018/08/RIAA_RI_Renchmark_Report_AUS_2018v8.pdf

It is perhaps unsurprising that investment managers adopt differing approaches to managing ESG risks in their portfolios. Some see this as a hygiene factor reflected in a page on their website that sets out a policy reflecting a broad approach to regulatory compliance and managing the risk of ESG impacts. However, others view it as an opportunity to build their entire investment process around an ethical framework. Instead of a mere marketing tool, they see a way to achieve environmental or social outcomes while delivering long-term value to investors.

This variety of approaches was reflected in the recent Global Impact Investor Network survey that showed 66% of impact investment managers principally target risk-adjusted market rate returns. This implies that they are unwilling to accept a below-market return while pursuing ESG focussed investments. However, investment opportunities are available that deliver positive environmental and social outcomes alongside return expectations; hence impact investors can be values driven whilst also seeking positive investment outcomes.

Making a positive impact

The traditional approach to ESG investing has been based upon excluding from the investable universe those companies that fail a screening process. In practice such companies are those whose activities are likely to cause harm to society or the environment, calling into question the long-term sustainability of their business model and earnings stream.

Such businesses might rely on the sale of tobacco or weaponry, pollute the environment, make an unacceptable contribution to climate change or carelessly manage their supply chain at the cost of vulnerable workers.

Such an approach represents progress upon traditional standard investing techniques, but investor thinking in this area has since progressed further. Some investors now increasingly expect their investments to make a positive impact on the wider world.

Impact investing might include equity investment in a developer of green energy technology, private equity investment in educational services, green bonds that finance wind farms or real estate investments that are both low energy and serve a social purpose such as aged care or social housing.

Real estate managers can go further and make a positive impact by investing in solar power. Shopping centres that use most of their energy during the day – when it is typically sunny – represent a solar power opportunity. However industrial premises, such as warehouses, tend to have more modest energy requirements and currently have limited solar generation potential. This is because exporting excess solar power into the grid is not remunerated at the same rate as drawing it down from the grid. Hence solar systems are generally sized to meet the energy demand of the building, rather than the maximum generation potential.

Managing ethical issues

A particular challenge of ESG investing is the divergence in thinking across institutions when considering the societal and environmental impacts of their investment activities. It is uncommon for two different investment policies to contain identical exclusions or even philosophies towards investing.

In particular, ESG investors may focus on a narrow or broad range of issues. Viewing the investment universe through a narrow lens is less common, however investors with a broader range of concerns are likely to hold different levels of concern and different priorities.

Carbon emission minimization for example, is typically a key feature of ESG investing, however policies vary significantly from those institutions that screen out only the most egregious emitters of CO2 to those that demand zero carbon emissions from all companies in which they invest.

Issues that tend to enjoy a high level of investor consensus include tobacco and prohibited weapons, such as chemical, biological, cluster munitions and land mines. There is widespread agreement amongst ESG investors that such products do unacceptable harm and that they should not invest in businesses whose primary purpose centres on their production.

However, there is greater ambiguity when businesses engage in excluded activities, but only as an incidental part of their overall business operations. An example might be a diversified mining company that provides essential raw products that are widely used, such as iron ore, aluminium and copper, but also engages in coal mining. It is now widely accepted that coal mining and its subsequent burning in power generation contributes to harmful climate change. Whereas a committed ethical investor would screen out such companies, an ESG risk focussed investor might consider them further if they had overall strong ESG characteristics. These might include mining efficiently and remediating mine sites upon the completion of operations.

Other areas where investors are likely to adopt differing positions are in the fields of animal rights or human rights. Investor attitudes towards such issues depend on values, which are likely to vary materially from one investor to another. Whereas ESG investing is based on scientific evidence correlating environmental or social harm with a business activity, an ethical approach rests upon a values framework which might be driven by a desire to avoid all harm to animals.

Managing supply chains in a responsible way has been a key ESG priority since the 2013 Rana Plaza disaster when 1,134 garment workers were killed in a building collapse in Bangladesh. The expectation that companies source supplies ethically is widely held. Most well governed companies understand the risks to their business in the form of operational disruption and reputational damage, which may occur if something goes wrong in the supply chain. However, investors do expect fund managers to engage with companies and to endeavor to hold them accountable for their supply chain practices.

Governance is another area of ESG investing where investor expectations and manager priorities vary. Diversity, executive pay, shareholder rights and board independence are all key areas which require engagement by investment managers. However, the relative importance that investors attach to different aspects of the governance process will depend on perceptions of long-term value that can be created through such a focus.

1 The Global Impact Investment Network (GIIN): Global Impact Investor Survey 2017, (2018), p3 https://thegiin.org/research/publication/annualsurvey2017

Source: AMP Capital 25 October 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Four global investment opportunities amid market uncertainty

In a time of market uncertainty with concerns around rising US interest rates and overvalued equities it can be difficult to find investment opportunities and it’s of little surprise that investors are asking where they should allocate their funds.

But the good news is that recent developments have highlighted and reinforced a number of investment opportunities around the world that we

Read MoreIn a time of market uncertainty with concerns around rising US interest rates and overvalued equities it can be difficult to find investment opportunities and it’s of little surprise that investors are asking where they should allocate their funds.

But the good news is that recent developments have highlighted and reinforced a number of investment opportunities around the world that we believe investors should be exploring. Four of our picks are detailed below.

1. Latin American and emerging markets

The first is Latin American and emerging markets.

Based on forward price to earnings ratios, the relative valuation of emerging markets equities versus US equities is reaching lows not seen since 2008. The US market is also showing signs of running out of breath, so we are selectively adding to our emerging markets allocations through Latin American equities, emerging market bonds, and certain currencies, including the Mexican Peso and the Chilean Peso.

Many Latin American currencies and markets have been under pressure thanks to uncertainty around the North American Free Trade Agreement (NAFTA), which creates a trade bloc between the US, Canada and Mexico. Latin American markets should have been benefiting from rising commodity prices but concerns that US President Donald Trump would dump the trade pact outweighed this.

The recently revised North American trade deal, now known as the United States Mexico Canada Agreement (USMCA), has removed that uncertainty. It comes shortly after the US revised its free trade agreement with South Korea (known as KORUS) and bodes well for upcoming US-Japan bilateral trade talks.

These recent agreements suggest that Washington seems happy to accept some minor modifications to existing free trade deals, declare victory and get ready for the midterm elections. This seems to be a win for free-trade ‘globalists’ and a loss for protectionists who want to restrict free trade and as a result, emerging markets, which are heavily exposed to trade and have borne the brunt of concerns around rising US protectionism, should benefit.

2. Chinese consumer stocks

The second opportunity is in Chinese consumer stocks.

The recent positive developments around US trade may point to the possibility of a deal being achieved with China, but I’m not so hopeful. It seems the US-China trade tension is a symptom of a much bigger problem: the Trump administration’s unease with the rising power of China.

I don’t expect to see a US-China trade deal soon but to offset weakening US exports, the Chinese will likely stimulate domestic demand through co-ordinated fiscal and monetary support which will benefit listed Chinese companies that are exposed to domestic consumer demand.

As a result, we are increasing our exposure to shares in mainland China-based companies that are traded in Renminbi on its domestic stock exchanges (China A shares) which are undervalued and should benefit from any monetary policy easing.

3. Energy

The third opportunity is in US and global energy, with oil likely to push higher towards $US80 a barrel before a brief pause.

On the supply side, Donald Trump has called on Saudi Arabia to lift production, but the reality is the Saudis have very little spare production. Supply from Iran is also likely to leave the market as the US wants all oil imports from Iran to end by November. In support of this, India (the second largest buyer of Iran’s oil after China) is reducing its intake of Iranian oil, cutting its purchases to zero in November. Meanwhile in the US, shale oil productivity has been declining and capital expenditure has collapsed after the 2015/16 energy crisis.

On the demand side, global growth is running at a solid pace despite the recent non-US softness. Chinese growth should see a rebound as the impact of recent policy easing comes through.

4. Japanese equities and banks

The final opportunity is in Japanese equities, and in particular Japanese banks.

The Japanese Government Pension Investment Fund (GPIF), which is the world’s largest retirement savings pool, recently announced it wouldn’t automatically reinvest redemptions into Japanese Government Bonds (JGBs).

We believe this is important because it indicates a cautious stance towards holding JGBs. The bond bubble is slowly deflating and the GPIF is rightly looking for flexibility rather than blindly adding bonds to its portfolio. Basically, demand for bonds is waning which suggests bond yields are likely to rise (when bond prices fall, yields rise).

At the same time, the Bank of Japan’s (BoJ) balance sheet will soon be as large as Japan’s GDP. The BoJ – Japan’s central bank – will have to taper or reduce purchases of JGBs to avoid further serious market distortions.

We believe Japanese banks are likely to be significant winners from this situation, with a flow-on effect to global banks.

A world of opportunity

In summary, for investors willing to explore global opportunities and consider different asset classes, there are a significant number of possibilities to diversify their portfolios, protect against the mature US bull market, and enhance returns so they can reach their investment objectives and goals.

Author: Nader Naeimi, Head of Dynamic Markets and Portfolio Manager of Dynamic Markets Fund

Source: AMP Capital 01 November, 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Three reasons why we’re not in a bear market

https://vimeo.com/299367257

October was certainly a volatile month for investors. Share markets globally fell between 6% and 7% in total return terms. Australia had the worst monthly outcome since August 2015.

But if you measure the falls from highs this year to recent lows the retreat has been even bigger. The average decline for global shares has been around 10%.

From its peak in

Read More

https://vimeo.com/299367257

October was certainly a volatile month for investors. Share markets globally fell between 6% and 7% in total return terms. Australia had the worst monthly outcome since August 2015.

But if you measure the falls from highs this year to recent lows the retreat has been even bigger. The average decline for global shares has been around 10%.

From its peak in late August, the S&PASX200 fell almost 11%. Emerging markets were hard hit, down around 20%, with China’s stock market slumping 30%.

Thankfully a bit of good news at the end of the month meant share markets have bounced around 3%.

The question now is, have we seen the bottom in markets?

We think it’s too early to say given various risks and so another bout of volatility remains possible. However, there are several reasons to believe that there is a good chance that markets will be higher in two months, six months or 12 months. In other words, I think the recent rout is likely a correction or a minor bear market within an ongoing bull market.

1. A bull market correction

The first reason is that for a major bear market to develop, where markets fall 20%, and the following year are down another 20% – as happened in the global financial crisis – you really need to see the US economy going into recession and dragging the rest of the world down with it. At the moment there is no sign of that happening.

2. Rates remain low

The second reason is that we’re in a world of relatively low interest rates. Yes, the US Federal Reserve is raising interest rates, but they have a long way to go before you could say interest rates are painful. And other countries are still a long, long way from raising interest rates. If anything, countries like Australia may still engage in monetary stimulus.

3. Normal volatility

The final reason is purely technical. We often see weakness around October. It is known as a volatile month. The good news is we typically rally into the end of the year and that strength continues into the early New Year. So, what we have seen in October is typical of seasonal volatility we get around this time of the year. It usually starts around August and September, but this year it started a little bit later in October.

Not the start of a major bear market

A number of worries triggered the recent sell-off, including US inflation, rising US rates, the China/US trade war, and concerns about emerging markets and Europe.

A lot of those worries still exist and markets could still have another leg down, retesting the lows we saw a few weeks ago. But I don’t think the recent sell-off represents the start of a major bear market. For that to develop we’d need to get a bit more negativity on the US economy and at this stage the US economy still remains pretty strong.

Source: AMP Capital 08 November, 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

13 common sense tips to help manage your finances

A few months ago Reserve Bank Governor Phillip Lowe provided four common sense points we should all keep in mind regarding borrowing to finance a home. (The Governor’s speech can be found here). I thought they made sense and so summarised them in a tweet to which someone replied that every checkout operator knows them. Which got me thinking that

Read MoreA few months ago Reserve Bank Governor Phillip Lowe provided four common sense points we should all keep in mind regarding borrowing to finance a home. (The Governor’s speech can be found here). I thought they made sense and so summarised them in a tweet to which someone replied that every checkout operator knows them. Which got me thinking that maybe many do know them, but a lot don’t, otherwise Australians would never have trouble with their finances. So I thought it would be useful to expand Governor Lowe’s list to cover broader financing and investment decisions we make. I have deliberately kept it simple and in many cases this draws on personal experience. I won’t tell you to have a budget though because that’s like telling you to suck eggs.

1. Shop around

We often shop around to get the best deal when it comes to consumer items but the same should apply to financial services. As Governor Lowe points out “don’t be shy to ask for a better deal whether for your mortgage, your electricity contract or your phone plan”. The same applies to your insurance, banking, superannuation, etc. It’s a highly-competitive world out there and financial companies want to get and keep your business. So when getting a new financial service it makes sense to look around. And when it comes time to renew a service – say your home and contents insurance – and you find that the annual charge has gone up way in excess of inflation (which is currently around 2%) it makes sense to call your provider to ask what gives. I have often done this to then be offered a better deal on the grounds that I am a long-term loyal customer.

2. Don’t take on too much debt

Debt is great, up too a point. It helps you have today what you would otherwise have to wait till tomorrow for. It enables you to spread the costs associated with long term “assets” like a home over the years you get the benefit of it and it enables you to enhance your underlying investment returns. But as with everything you can have too much of it. Someone wise once said “it’s not what you own that will send you bust but what you owe.” So always make sure that you don’t take on so much debt that it may force you to sell all your investments just at the time you should be adding to them or worse still potentially send you bust. Or to sell your house when it has fallen in value. A rough guide may be that when debt servicing costs exceed 30% of your income then maybe you have too much debt – but it depends on your income and expenses. A higher income person could manage a higher debt servicing to income ratio simply because living expenses take up less of their income.

3. Allow that interest rates can go up as well as down

Yeah, I know that it’s a long time since offical interest rates were last raised in Australia – in fact it was way back in 2010. So as Governor Lowe observes “many borrowers have never experienced a rise in official interest rates”. But don’t be fooled by the recent history of falling or low rates. My view is that an increase in rates is still a long way off (and they may even fall further first) – but that’s just a view and views can be wrong. History tells us that eventually the interest rate cycle will turn up. Just look at the US where after six years of near zero interest rates, official US interest rates have risen 2% over the last three years. So, the key is to make sure you can afford higher interest payments at some point. And when official rates move up the moves tend to be a lot larger than the small out of cycle moves from banks that have caused much angst lately.

4. Allow for rainy days

This is another one raised by Governor Lowe who said: “things don’t always turn out as we expect. So for most of us having a buffer against the unexpected makes a lot of sense.” The rainy day could come as a result of higher interest rates, job loss or an unexpected expense. This basically means not taking all the debt offered to you, trying to stay ahead of your payments and making sure that when you draw down your loan you can withstand at least a 2% rise in interest rates.

5. Credit cards are great, but they deserve respect

I love my credit cards. They provide me with free credit for up to around 6-7 weeks and they attract points that can really mount up (just convert the points into gift cards and they make optimal Christmas presents!). So, it makes sense to put as much of my expenses as I can on them. But they charge usurious interest rates of around 20-21% if I get a cash advance or don’t pay the full balance by the due date. So never get a cash advance unless it’s an absolute emergency and always pay by the due date. Sure the 20-21% rate sounds a rip-off but don’t forget that credit card debt is not secured by your house and at least the high rate provides that extra incentive to pay by the due date.

6. Use your mortgage for longer term debt

Credit cards are not for long term debt, but your mortgage is. And partly because it’s secured by your house, mortgage rates are low compared to other borrowing rates – at around 4-5% for most. So if you have any debt that may take longer than the due date on your credit card to pay off then it should be on your mortgage if you have one.

7. Start saving and investing early

If you want to build your wealth to get a deposit for a house or save for retirement the best way to do that is to take advantage of compound interest – where returns build on returns. Obviously, this works best with assets that provide high returns on average over long periods. But to make the most of it you have to start as early as possible. Which is why those piggy banks that banks periodically hand out to children have such merit in getting us into the habit of saving early.

Of course, this gives me an opportunity to again show my favourite chart on investing which tracks the value of $1 invested in Australian shares, bonds and cash since 1900 with dividends and interest reinvested along the way. Cash is safe but has low returns and that $1 will have only grown to $237 today. Shares are volatile (& so have rough periods highlighted by arrows) but if you can look through that they will grow your wealth and that $1 will have grown to $526,399 by today.

Source: Global Financial Data, AMP Capital

8. Allow that asset prices go up and down

It’s well known that the share market goes through rough patches. The volatility seen in the share market is the price we pay for higher returns than most other asset classes over the long term. But when it comes to property there seems to be an urban myth that it never goes down in value. Of course property prices will always be smoother than share prices because it’s not traded daily and so is not subject to daily swings in sentiment. But history tells home prices do go down as well as up. Japanese property prices fell for almost two decades after the 1980s bubble years, US and some European countries’ property values fell sharply in the GFC and the Australian residential property market has seen several episodes of falls over the years and of course we are going through one right now. So the key is to allow that asset prices don’t always go up – even when the population and the economy are growing.

9. Try and see big financial events in their long-term context

Hearing that $50bn was wiped off the share market in one day sounda scary – but it tells you little about how much the market actually fell and you have only lost something if you actually sell out after the fall. Scarier was the roughly 20% fall in share markets through 2015-16 and worse still the GFC that saw roughly 50% falls. But such events happen every so often in share markets – the 1987 crash saw a 50% in a few months & Australian shares fell 59% over 1973-74. And after each the market has gone back up. So, we have seen it all before even though the details may differ. The trick is to allow for periodic sharp falls in your investment strategy and when they do happen remind yourself that we have seen it all before and the market will find a base and resume its long-term rising trend.

10. Know your risk tolerance

When embarking on investing it’s worth thinking about how you might respond if you found out that market movements had just wiped 20% off the value of your investments. If your response is likely to be: “I don’t like it, but this sometimes happens in markets and history tells me that if I stick to my strategy I will see a recovery in time” then no problem. But if your response might be: “I can’t sleep at night because of this, get me out of here” then maybe you should rethink your strategy as you will just end up selling at market bottoms and buying tops. So try and match your investment strategy to your risk tolerance.

11. Make the most of the Mum and Dad bank

The housing boom in Australia that got underway in the mid-1990s and reached fever pitch in Sydney & Melbourne last year has left housing very unaffordable for many. This contributed to a huge wealth transfer from Millennials to Baby Boomers and some Gen Xers. Hopefully the current home price correction underway will help in starting to correct that. But for Millennials in the meantime, if you can it makes sense to make the most of the “Mum and Dad bank”. There are two ways to do this. First stay at home with Mum and Dad as long as you can and use the cheap rent to get a foot hold in the property market via a property investment and then using the benefits of being able to deduct interest costs from your income to reduce your tax bill to pay down your debt as quickly as you can so that you may be able to ultimately buy something you really want. (Of course, changes to negative gearing if there is a change to a Labor Government could affect this.) Second consider leaning on your parents for help with a deposit. Just don’t tell my kids this!

12. Be wary of what you hear at parties

A year ago Bitcoin was all the rage. Even my dog was asking about it – but piling in at around $US19,000 a coin just when everyone was talking about it back then would not have been wise (its now below $US6500) even though many saw it as the best thing since sliced bread. Often when the crowd is dead set on some investment it’s best to do the opposite.

13. There is no free lunch

When it comes to borrowing & investing there is no free lunch – if something looks too good to be true (whether it’s ultra-low fees or interest rates or investment products claiming ultra-high returns & low risk) then it probably is and it’s best to stay away.

Concluding comment

I have focussed here mainly on personal finance and investing at a very high level, as opposed to drilling into things like diversification and taking a long-term view to your investments. An earlier note entitled “Nine keys to successful investing” focussed in more detail on investing and can be found here.

Source: AMP Capital 15 November 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.