Provision Newsletter

Monetary Policy Decision – Statement by Philip Lowe, RBA Governor, October 2018

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial

Read MoreAt its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased due to both higher oil prices and some lift in wages growth. A further pick-up in inflation is expected given the tight labour markets, and in the United States, the sizeable fiscal stimulus. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions in the advanced economies remain expansionary, although they are gradually becoming less so in some countries. Yields on government bonds have moved a little higher, but credit spreads generally remain low. There has been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates are higher than they were at the start of the year, although they have declined since the end of June. In response, some lenders have increased their standard variable mortgage rates by small amounts, while at the same time reducing mortgage rates for some new loans.

The latest national accounts confirmed that the Australian economy grew strongly over the past year, with GDP increasing by 3.4 per cent. The Bank’s central forecast remains for growth to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Growth in household income remains low and debt levels are high. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years due to rises in some commodity prices. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, but it has depreciated against the US dollar along with most other currencies.

The outlook for the labour market remains positive. The unemployment rate is trending lower and, at 5.3 per cent, is the lowest in almost six years. The vacancy rate is high and there are reports of skills shortages in some areas. A further gradual decline in the unemployment rate is expected over the next couple of years to around 5 per cent. Wages growth remains low, although it has picked up a little. The improvement in the economy should see some further lift in wages growth over time, although this is likely to be a gradual process.

Inflation is around 2 per cent. The central forecast is for inflation to be higher in 2019 and 2020 than it is currently. In the interim, once-off declines in some administered prices in the September quarter are expected to result in inflation in 2018 being a little lower than otherwise.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Growth in credit extended to owner-occupiers remains robust, but demand by investors has slowed noticeably as the dynamics of the housing market have changed. Credit conditions are tighter than they have been for some time, although mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Source: Reserve Bank of Australia, October 2nd, 2018

Enquiries

Media and Communications

Secretary’s Department

Reserve Bank of Australia

SYDNEY

Phone: +61 2 9551 9720

Fax: +61 2 9551 8033

Email: rbainfo@rba.gov.au

Successful investing despite 115 million worries and Truth Decay – how to turn down the noise

“Information is not knowledge, knowledge is not wisdom – Frank Zappa (and maybe some others)”

It may seem that the worry list for investors is bigger and more confusing than ever before. Some of this may relate to US President Trump’s disruptive and “open mouth” approach as highlighted by the “trade war” and his frequent and sometimes contradictory tweets. For example,

Read More“Information is not knowledge, knowledge is not wisdom – Frank Zappa (and maybe some others)”

It may seem that the worry list for investors is bigger and more confusing than ever before. Some of this may relate to US President Trump’s disruptive and “open mouth” approach as highlighted by the “trade war” and his frequent and sometimes contradictory tweets. For example, on 24th July Trump tweeted “Tariffs are the greatest!” But 12 hours later he tweeted “The European Union is coming to Washington tomorrow to negotiate a deal on Trade. I have an idea for them. Both the U.S. and the E.U. drop all Tariffs, Barriers and Subsidies!”

Now I think I know where he was coming from, but all this noise can create a lot of uncertainty for investors. But noise around Trump is part of a broader issue around information overload and broader again in terms of what a report by the RAND Corporation – a US non-partisan research organisation – has called Truth Decay. As we have observed in recent years there seems to be a never-ending worry list for investors that is receiving greater prominence as the information age enables the ready and rapid dissemination of news and opinion. But we need to recognise that much of this is just noise and ill-informed and that there is a big difference between information and wisdom when it comes to investing. The danger is that information and opinion overload is making us all worse investors as we lurch from one worry to the next resulting in ever shorter investment horizons in the process.

“Just remember: What you’re seeing and what you’re reading is not what’s happening.” – President Donald Trump

Truth Decay – what is it & what are its consequences?

Truth Decay as analysed by the RAND Corporation report is characterised by: disagreement about facts and their analytical interpretation; a blurring between fact and opinion; an increase in the volume and influence of opinion and personal experience over fact; and declining trust in traditional sources of facts such as government and newspapers. It’s evident in: declining support for getting children vaccinated despite medical evidence supporting it; perceptions crime has increased when it’s actually declined; and a lack of respect for scientific evidence around global warming. Elements of Truth Decay were evident in past periods like the 60s & 70s, but increasing disagreement about facts makes the current period different.

The causes of Truth Decay include: behavioural biases that leave people susceptible to information and opinion that confirms their views and aligns with their personal experience; the information revolution and social media that have led to a surge in the availability of information and opinion and the rise of partisan news channels; educational systems that have not taught us to be critical thinkers; social polarisation with rising inequality and division attracting people to opposing sides that are reinforced by participating in social media echo chambers. The consequences include a deterioration in civil debate as people simply can’t agree on the facts, political paralysis, disengagement from societies’ institutions and uncertainty.

Why is Truth Decay relevant for investors?

Truth Decay is relevant for investors because: it could lead to less favourable economic policy decisions which could weigh on investment returns; and investors are subject to the same forces driving Truth Decay such that it explains why the worry list for investors seems more worrying and distracting. The first is a topic for another day, but in terms of the heightened worry list facing investors there are three key drivers.

First, just as with the broader concept of Truth Decay various behavioural biases leave investors vulnerable in the way they process information. In particular, they can be biased to information and particularly opinions that confirm their own views. People are also known to suffer from a behavioural trait known as “loss aversion” in that a loss in financial wealth is felt much more distastefully than the beneficial impact of the same sized gain. This likely owes to evolution which has led to much more space in the human brain devoted to threat than reward. As a result, we are more predisposed to bad news stories that alert us to threat as opposed to good news stories. In other words bad news and doom and gloom find a more ready market than good news or balanced commentary as it appeals to our instinct to look for risks. Hence the old saying “bad new sells”.

Secondly, thanks to the information revolution we are now exposed to more information than ever on both how our investments are going and everything around them. This has particularly been the case since the GFC – the first iPhone was only released in 2007! In some ways this is great as we can check facts and analyse things very easily. But the downside is that we have no way of assessing all the extra information and less time to do so. So, it can become noise at best, distracting at worst. If we don’t have a process to filter it and focus on what matters we can simply suffer from information overload. This can be bad for investors as when faced with too much information we can become more uncertain, freeze up and make the wrong investment decisions as our natural “loss aversion” combines with what is called the “recency bias” that sees people give more weight to recent events which can see investors project bad news into the future and so sell after a fall.

But the explosion in digital/social media means we are bombarded with economic and financial news and opinions with 24/7 coverage by multiple web sites, subscription services, finance updates, TV channels, social media feeds, etc. And in competing for your attention, bad news and gloom trumps good news and balanced commentary as “bad news sells.” And the more entertaining it is the more attention it gets, which means less focus on balanced quality analysis. An outworking of all this is that the bad news seems “badder” and the worries more worrying. Google the words “the coming financial crisis” and you get 115 million search results with titles such as:

-

a vicious Fed-fuelled economic crisis is coming

-

coming financial crisis: a look behind the wizard’s curtain

-

here comes another global financial crisis

-

coming financial crisis will be much worse than Great Depression

-

another financial crisis is imminent, four reasons why

-

Japanese whales and the next financial crisis – I knew there was a connection!

In the pre-social media/pre-internet days it was much harder for ordinary investors to be exposed to such disaster stories on a regular basis. The obvious concern is that the combination of a massive ramp up in information and opinion combined with our natural inclination to zoom in on negative news is making us worse investors: more distracted, fearful, reactive and short-term focussed and less reflective and long-term focussed.

Five ways to manage information & opinion overload

To be a successful investor you need to make the most of the power of compound interest and to do that you need to invest for the long term and not get blown around by each new worry. And the only way to do that is to turn down the noise on the worry list. This is getting harder given the distractions on social media. But here are five suggestions as to how to do so:

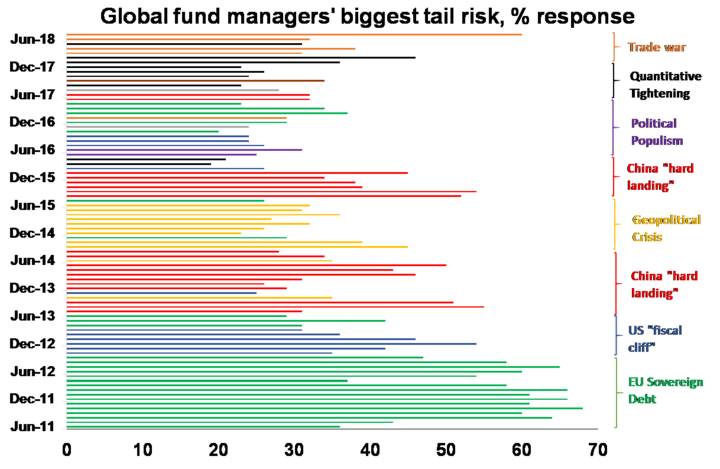

First, put the latest worry in context. There is always an endless stream of worries. Here’s a list of the main worries of the last five years: Fed tapering; the US Government shutdown; Ukraine; IS terror threat; Ebola; deflation; Greece & Eurozone debt; China worries; Australian recession fears, property & banks; Brazil and Russia in recession; oil price collapse; manufacturing slump; Fed raising rates; falling profits; Brexit; Trump; North Korea; South China Sea tensions; Italy; and trade wars. Even fund managers go from one worry to another as evident in the next chart that tracks what they nominate as the biggest risk over time.

click to enlarge

Source: BofA Merrill Lynch Global Fund Manager Survey, AMP Capital

Yet despite all the worries, investment returns have been good with, eg, average balanced superannuation funds returning 8.5% pa over the last five years. The global economy has had plenty of worries over the last century, but Australian shares still returned 11.8% pa since 1900 and US shares 9.8% pa.

Source: ASX, AMP Capital

Some of the worries we hear much about come to something big, but most of the time they don’t with US and Australian shares rising seven and eight years out of 10 respectively since 1900. So is the latest worry is any more threatening than the last one?

Second, recognise how markets work. Shares return more than cash in the long term because they can lose money in the short term. So, while the share market is highly volatile in the short term – often in response to loss-averse investors projecting recent bad news and worries into the future – it has strong returns over rolling 20-year periods. Short-term volatility is the price wise investors pay for higher long-term returns.

Third, find a way to filter news so that it doesn’t distort your investment decisions. For example, this could involve building your own investment process or choosing a few good investment subscription services and relying on them.

Fourth, don’t check your investments so much. On a day to day basis the Australian All Ords price index and the US S&P 500 price index are down almost as much as they are up. See the next chart. So, it’s a coin toss as to whether you will get good news or bad on a day to day basis. By contrast if you only look at how the share market has gone each month and allow for dividends the historical experience tells us you will only get bad news about 35% of the time. And if you stretch it out to each decade, since 1900 positive returns have been seen 100% of the time for Australian shares and 82% for US shares.

Data from 1995 and 1900. Source: Global Financial Data, AMP Capital

So, the less you look the less you will be disappointed and so the lower the chance that a bout of “loss aversion” will be triggered which leads you to sell at the wrong time.

Finally, look for opportunities that bad news and investor worries throw up. Periods of share market turbulence after bad news provide opportunities for smart investors as such periods push shares into cheap territory.

Source: AMP Capital 28 September 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Introducing Sonia Baillie

Sonia Baillie, Head of Credit and Portfolio Manager of the AMP Corporate Bond Fund, shares how investing in fixed income can benefit investors and what her investment philosophy is.

Source: AMP Capital September 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital

Read MoreSonia Baillie, Head of Credit and Portfolio Manager of the AMP Corporate Bond Fund, shares how investing in fixed income can benefit investors and what her investment philosophy is.

Source: AMP Capital September 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Why the world of retail is changing

In the first of our two-part analysis of the changing face of retail, our team of experts look at some longer-term social trends and explain how these are changing the way that we shop and visit malls.

Q. What changes are impacting commercial real estate?Commercial real estate is going through rapid change as people become consumers of space, not just of

Read MoreIn the first of our two-part analysis of the changing face of retail, our team of experts look at some longer-term social trends and explain how these are changing the way that we shop and visit malls.

Q. What changes are impacting commercial real estate?

Commercial real estate is going through rapid change as people become consumers of space, not just of products and services.

This is being driven by three macro trends that are transforming the way in which societies utilise space:

-

Urbanisation – Between 75% – 80% of the world’s population will live in cities within the next 30 years, according to studies by the UN and IMF. This will raise accessibility issues when pressure on transport infrastructure increases as people move closer to work in order to reduce commute times.

The implication of this is that building design will become more agile and be more sustainable. More mixed-use buildings are being completed; these are already common in major Asian commercial centres but are now starting to appear more in Australia. Previously an office block might have some ground-floor retail space, however new designs increasingly include hotels, apartments, leisure facilities and co-working spaces.

-

Flexible working – The second trend is the changing nature of office work. Baby boomers entered the workforce at a time when a closed individual office provided solitude and status. By the time they reached management positions, open-plan working was the norm. Now this demographic sets the tone of businesses, the focus is switching to flexible working, home working and co-working spaces.

A more agile approach aligns well with millennials whose embrace of hierarchy and structure is rather less than previous cohorts – and also with employees who place a high priority on family life.

This shift coincides with a period when office rental levels are at historic highs in some Australian cities.

-

Technology – The final trend driving change is the consumer’s higher expectations of the accessibility of instant and relevant information via mobile technology. Retail and other commercial centres in Australia have traditionally not managed customer information well. However, it is expected they will increasingly focus on integrating the analysis of data into their operating models.

Q. What shops and other facilities do shoppers expect to see in centres?

Customers want to be able to do more than just buy something when they visit a shopping centre. Now, they expect a space in which they can connect with friends and family; simply providing a food court will no longer suffice. Successful shopping centres now offer a mix of higher-range casual dining venues, trendy bars and cinema complexes.

Families are attracted by children’s play areas and high-quality baby changing facilities; this may extend to childcare and even educational facilities. Fitness centres, spas, wellness outlets and medical services drive further footfall.

The unifying feature is that consumers are more likely to be attracted to sources of value that cannot easily be reproduced and disrupted online. This even includes the more humble and longer-established dry cleaner, mobile phone repair or key-cutting kiosks. Once established as a destination that successfully attracts the target demographic, a centre and its retail tenants are then much better positioned to profitably transact physical goods.

Consumers are demanding an experience that is exciting or surprising and based upon a human element.

Q. When do people shop online and when do they want to visit a shopping centre?

For most consumers in Australia this is not an either/ or question as people transact through both channels at different times. However, the experience for the online or physical shopper is likely to determine whether the market proposition is a success.

Commentary on the trends in retail sometimes suggests that e-commerce is a recent evolution, however online shopping sites have now been transacting in Australia for 20 years. During this time there has been no fall in annual mall visits, however the challenge for those in the wider retail environment is to persuade these visitors to part with their money.

In Australia the market is structured in such a way that scope for product differentiation is somewhat limited and hence it is the quality and nature of the experience that represents the point of difference. In order to attract visitors, a shopping centre must be seen as a place of gathering as much as a place of commerce. It must be about an experience that is valued beyond the sum of any transactions, in which the opening of our wallets is a mere by-product of an engaging and sociable experience.

In the second article our team analyse how shopping centres might adapt to this changing environment and consider ways in which investors might best position their portfolios to take advantage of evolving consumer preferences.

Source: AMP Capital September 2018

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Investing in disruption: Part One

Disruption is a term that is used widely. But what does it really mean when it comes to investing?

This is the first in a series of articles that explores what disruption really means, exploring examples of leading disruptive companies, and implications for investors.

It’s easy to assume disruption is just another business buzzword. But the notion of disruption really speaks to

Read MoreDisruption is a term that is used widely. But what does it really mean when it comes to investing?

This is the first in a series of articles that explores what disruption really means, exploring examples of leading disruptive companies, and implications for investors.

It’s easy to assume disruption is just another business buzzword. But the notion of disruption really speaks to ongoing economic evolution. It’s at the heart of human nature and has been around for centuries.

Importantly, disruption benefits the economy because it leads to efficiencies by reducing costs, introducing new goods and services, as well as fast-tracking and improving business outcomes. Historically it has also been a net creator of jobs rather than a job killer.

Additionally, disruption is usually a positive force in society. Lower costs lead to higher living standards and supports economic development. It’s also not new. The long transition from manual to machine-led agriculture is a good example.

In 1837 John Deere invented the steel plow, which transformed farming as we know it. There have subsequently been scores of disruptive technologies in agriculture including combine harvesters and tractors. Today, the use of drones and data continues to transform agriculture, leading to massive improvements in productivity and efficiency. This process will only continue over time.

However, innovations stemming from disruption can take time to take hold. The automobile is an example. Invented in 1885, for many decades it remained an unaffordable luxury. Now, cars are ubiquitous. Cost is a major reason innovations such as the car take time to become widespread. Initially, a car cost many times the average person’s annual income. Now, the cost of a car is a fraction of this amount and affordable for many.

Now, the pace of disruption is increasing thanks to technology. The music industry is a good example. Vinyl records were the dominant music delivery mechanism for many years. Then, cassettes were invented, and the two co-existed for some time. Along came CDs and rendered cassettes and records largely obsolete. Mini discs improved on CDs, until the invention of the iPod transformed music once more. We now stream music from our smartphones, demonstrating how technology can accelerate the pace of disruption and transform an industry and competitive landscape.

So, music is a great example of how the pace of disruption has accelerated, particularly when it involves technology. Technology makes acceleration possible because it has increased the speed and reduced the cost of innovation in many industries through the ever-reducing cost of processing power that has facilitated and enabled more digital disruption. This explains why the nature of a company’s competitive advantage and the pace of disruption has changed over time. In the digital revolution, core assets are more often than not intangible in nature such as Intellectual Property and network effects as opposed to the physical assets such as plant and machinery that dominated the non-digital era.

Ultimately this has important ramifications for long-term investing, which we will explore in future articles, including the nature and durability of competitive advantage, identification of sustainable long-term growth trends, and corporate capital allocation.

Source: AMP Capital 18 Septemebr 2018

Author: Simon Steele, Head of Global Equities London, United Kingdom

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Are the troubles in Turkey easing?

https://vimeo.com/289814747

Investors may be eyeing off value in emerging markets after the recent sell-off triggered by concerns about the Turkish economy.

Emerging market (EM) shares in local currency terms are down around 14% from their January high, and emerging market currencies are down 16% since their February high.

Emerging markets are now trading on a forward PE of around 11 times, making them

Read More

https://vimeo.com/289814747

Investors may be eyeing off value in emerging markets after the recent sell-off triggered by concerns about the Turkish economy.

Emerging market (EM) shares in local currency terms are down around 14% from their January high, and emerging market currencies are down 16% since their February high.

Emerging markets are now trading on a forward PE of around 11 times, making them quite cheap, as are their currencies.

But the troubles in Turkey, which have prompted its equity markets and currencies to tumble, are likely to continue as the underlying problems in its economy persist.

Turkey is experiencing very high rates of inflation and its central bank is probably going to have to raise rates further to combat that. So, the volatility and uncertainty around Turkey will continue.

Contagion

The real problem is the contagion effect those concerns have on other emerging market countries. As we have seen in the past, when one emerging market gets into trouble, investors look around for others that might be in trouble too.

The concerns around Turkey have already spread to Argentina; investors are worried the problems will also spread to Brazil and other emerging markets, which is weighing on their shares and currencies.

Foreign investors are happy to put money into emerging markets during good times but they’re now fretting those countries may not be able to service their loans, particularly if they have borrowed in $US.

The US is raising rates, which continues to put upward pressure on the $US, making it more expensive to service loans in that currency.

Investors have other concerns too around emerging countries’ vulnerability to the threat to global trade, and uncertainty around slowing growth in the Chinese economy.

Good value

When you throw in worries about specific countries like Turkey it creates ongoing issues around emerging markets. This means that worries about emerging markets will probably continue for a little while yet.

There is good value in emerging markets if you take a longer-term, say a five-year, view. But investors need to be aware that we may see some more downside in the short term before we ultimately bottom out in these markets.

From a historical perspective, the declines we are currently seeing in emerging markets are mild. They crashed 27% in 2015-16 and they could fall further now if the $US continues to rise, making debt servicing harder in the emerging world.

Soucre: AMP Capital 18 Septemebr 2018

Author: Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Capital

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.