Olivers Insights

Where are we in the global investment cycle? What does this mean for investors?

It’s now a decade since the first problems with US sub-prime mortgages started to appear and nearly eight years since share markets hit their global financial crisis lows. From those lows in 2009 lows US shares are up 239%, global shares are up 167% and Australian shares are up 80% (held back by relatively higher interest rates, the

Read More  It’s now a decade since the first problems with US sub-prime mortgages started to appear and nearly eight years since share markets hit their global financial crisis lows. From those lows in 2009 lows US shares are up 239%, global shares are up 167% and Australian shares are up 80% (held back by relatively higher interest rates, the absence of money printing, the plunge in commodity prices from their 2011 highs and the high $A). An obvious question is how close the next downturn is, which ultimately relates to where we are in the investment cycle.

It’s now a decade since the first problems with US sub-prime mortgages started to appear and nearly eight years since share markets hit their global financial crisis lows. From those lows in 2009 lows US shares are up 239%, global shares are up 167% and Australian shares are up 80% (held back by relatively higher interest rates, the absence of money printing, the plunge in commodity prices from their 2011 highs and the high $A). An obvious question is how close the next downturn is, which ultimately relates to where we are in the investment cycle.

The long US cyclical bull market

Where we are in the investment cycle is particularly pertinent in relation to the US. The cyclical bull market in US shares that started in March 2009 will be eight years old in March. It’s the second longest cyclical bull market since World War Two in terms of time and the third strongest in terms of percentage gain. See the next table.

Cyclical bull markets in US shares since WW2

click to enlarge

I have applied the definition that a cyclical bull market is a rising trend in shares that ends when shares have a 20% or more fall (ie, a cyclical bear market). Source: Bloomberg, AMP Capital.

Similarly, according to the US National Bureau of Economic Research the current US economic expansion that started in June 2009 at 92 months old is the fourth longest since 1929 and compares to an average expansion of 70 months. With the US cyclical bull market and economic expansion both now long in the tooth, some fear that US shares are vulnerable to another bear market and by implication given the direction setting influence of the US share market, global and Australian shares would be vulnerable too. A related concern is that, with the US economic expansion already longer than normal, any stimulus that President Trump may provide risks overheating the US economy and much higher interest rates which could bring on a bear market.

The investment cycle

The next chart shows a stylised version of the investment cycle where the thick grey line represents the economic cycle.

The investment cycle

Source: AMP Capital

A typical cyclical bull market in shares has three phases:

-

Scepticism – Phase 1 normally starts when economic conditions are still weak and confidence is poor, but smart investors start to see value in shares helped by ultra easy monetary conditions, low interest rates and low bond yields.

-

Optimism – Phase 2 is driven by strengthening profits as economic growth turns up and investor scepticism gives way to optimism. While monetary policy may start to tighten, it is from very easy conditions and will remain easy as inflation remains low. Therefore, bond yields may drift higher but not enough to derail the cyclical bull market in shares.

-

Euphoria – Phase 3 sees investors move from optimism to euphoria helped by strong economic and profit conditions which pushes shares into overvalued territory. Meanwhile, strong economic conditions drive signs of economic excess – overinvestment, full capacity utilisation, surging private sector debt, high and surging inflation – which forces central banks to move into tight monetary policy, in turn pushing bond yields significantly higher. The combination of overvaluation, investors being fully loaded up on shares and tight monetary policy sets the scene for a new bear market.

Typically the bull phase lasts 3-5 years. But it varies depending on how quickly recovery precedes, excess builds up, inflation rises and extremes of overvaluation and investor euphoria appear. As a result “bull markets do not die of old age but of exhaustion”.

So where are we now in the investment cycle?

So right here the big question is: are we in the “euphoria” phase that ultimately leads to the “exhaustion” of the cyclical bull market in shares and the next bear market? The best way to look at this is to look at economic conditions, monetary conditions, share market valuation and investor sentiment and positioning:

Firstly, in terms of economic conditions it’s hard to argue we are in the “euphoria” phase. There are few signs of economic excess:

-

While headline inflation is rising globally this largely reflects the bounce in oil prices. Core inflation in major countries ranges between zero (Japan) to 1.7% (US), i.e. far from out of control.

-

After years of below trend growth globally, spare capacity still remains and this will constrain core inflation. Similarly wages growth remains depressed even in the US (at around 2.5% year on year) despite a tighter labour market.

Source: Bloomberg, AMP Capital

-

There is no sign of overinvestment globally – in fact there has been too little investment. While the US recovery is further advanced, even here business investment (excesses in which preceded the tech wreck) and residential property investment (excesses in which preceded the GFC) are around or below their long term averages relative to GDP.

Source: Thomson Reuters, AMP Capital

-

Overall private sector debt growth is modest in most countries (except for corporate debt in the US and China).

Secondly, global monetary conditions remain easy and in the absence of broad based excess (in growth, debt, or inflation) look likely to remain so. Yes the Fed is likely to hike rates more aggressively this year but it’s still from a very easy base and other central banks (including the RBA) are either on hold or easing. So a shift to tight money that brings an end to the economic cycle looks a fair way off.

Thirdly, share market valuations are mostly okay. Sure, measured in isolation against their own history shares are no longer cheap. In fact, forward price to earnings multiples in the US and Australia are above long term averages. However, once the gap between share market earnings yields and still low bond yields is allowed for, shares are fair value to cheap depending on the market (next chart).

Source: Bloomberg, AMP Capital

Fourthly, while short term investor sentiment is excessively bullish long term measures of positioning are not. In the US the huge investor flows into bond funds over the last few years have yet to reverse in favour of shares. In Australia sentiment towards shares as a wise destination for savings remains low and investors still prefer bank deposits. No euphoria here.

Source: Westpac/Melbourne Institute, AMP Capital

Finally, while the US cycle is more advanced, it could be argued that the 19% fall in US shares in mid-2011 was a bear market. So the bull market in US shares is perhaps not so old after all! Moreover, major non-US share markets and Australian shares did have a bear market in both 2011 and 2015-16 so their cyclical bull markets are not old at all. In this regard European and Japanese share markets are relatively attractive thanks to cheaper valuations and still dovish central banks.

Overall, we are still not seeing the signs of excess, euphoria and exhaustion that typically come at cyclical economic and share market peaks. So barring some sort of external shock, the cyclical bull market in shares looks like it still has further to go – particularly if global economic growth returns to more normal levels which in turn will help earnings.

With regard to any Trump fiscal stimulus, this analysis suggests there is still a bit of room for it before it causes the US economy to overheat. Particularly if the US dollar continues to trend higher, which takes some off the pressure of the Fed to raise rates. In any case it’s looking likely that fiscal stimulus in the US won’t hit till late this year and will unlikely to be more than 1% of US GDP given the constraints Congress is likely to impose. In fact the focus is more likely to be on providing a boost via economic reforms – deregulation, tax reform and inducements to invest – rather than traditional stimulus.

Investment implications

First, while corrections should be anticipated – with Trump and upcoming Eurozone elections being potential triggers – we still appear to be a long way from the peak in the investment cycle.

Second, non-US share markets and economies – notably Japan and Europe – are less advanced in their cycles and so provide opportunities for investors.

Source: AMP Capital 9 Feb 2017

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Is Donald Trump’s honeymoon with investors over?

Since the US election last November US and global shares rallied around 8% and Australian shares rallied around 12% to their recent highs. Related to this the US dollar, bond yields and some commodity prices also pushed significantly higher. Optimism regarding Donald Trump’s pro-growth policies were not the only factor playing a role in this rally – global

Read More  Since the US election last November US and global shares rallied around 8% and Australian shares rallied around 12% to their recent highs. Related to this the US dollar, bond yields and some commodity prices also pushed significantly higher. Optimism regarding Donald Trump’s pro-growth policies were not the only factor playing a role in this rally – global economic indicators have improved significantly in most regions – but it certainly played a role. With Trump now inaugurated as President we are at the point where that optimism is being tested.

Since the US election last November US and global shares rallied around 8% and Australian shares rallied around 12% to their recent highs. Related to this the US dollar, bond yields and some commodity prices also pushed significantly higher. Optimism regarding Donald Trump’s pro-growth policies were not the only factor playing a role in this rally – global economic indicators have improved significantly in most regions – but it certainly played a role. With Trump now inaugurated as President we are at the point where that optimism is being tested.

Donald Trump has only been President for two weeks but it seems that he has already done a lot with numerous major announcements. So far the key moves relate to: minimising the economic burden of Obamacare; reviewing new regulations; preventing non-government organisations that perform abortions from receiving Federal funding; withdrawing the US from the Trans Pacific Partnership free trade deal; freezing Federal hiring; moving towards approving the Dakota and Keystone XL oil pipelines; speeding up approvals for high priority infrastructure projects; reducing regulatory burdens facing manufacturers; directing the construction of a wall with Mexico; support for a “border adjustment tax”; and various restrictions around immigration – in particular a 90 day ban on travellers to the US from seven majority Islamic countries.

While these moves are basically consistent with his campaign policies, some have created considerable consternation in the US and globally. And Trump and his teams’ “thin skin” has led to various distractions – eg, around how many people attended his inauguration and “alternative facts”.

Initially investment markets reacted favourably after Trump’s inauguration as many of his orders were pro-business, but the travel ban has seen uncertainty creep in around whether the new administration knows what it is doing (the ban seems to have been poorly thought through in terms of implementation and legalities as it was not vetted by the bureaucracy first) and around how isolationist Trump is prepared to take the US. Quite clearly Trump is a different kind of US President to the norm. This note looks at the main issues of importance to investors.

Risks under President Trump

Donald Trump’s presidency comes with a number of risks:

-

He could make a major policy mistake – for example, some of his recent announcements don’t appear to have been well thought through (eg, the travel ban).

-

He could trigger a major global trade war which could adversely affect global growth. Or, in targeting countries with which the US runs a trade deficit and its NATO allies for not “paying their fair share”, he could threaten the flow of cheap funding that the US benefits from.

-

He could go the way of Nixon (impeachment, resignation) who was known for his thin skin and paranoia regarding the media – Trump seems to be making an enemy of much of the media who are no doubt likely to try and do their best to discredit him eg, around conflicts with his business interests, the Russian link or whatever.

-

His proposed fiscal stimulus risks a further budget and public debt blow out. When Ronald Reagan took over US public debt was 30% of GDP, now it’s over 100% and the budget deficit is likely to deteriorate in the years ahead thanks to the aging population. Or it could overstimulate the US economy causing a far more aggressive Fed.

-

Alternatively, Congressional constraints could mean that any fiscal stimulus is underwhelming and/or that he fails to relax the Dodd-Frank financial regulations. Achieving tax and spending changes will be easier for Trump as the Republicans have simple majorities in both houses of Congress which is all that’s required, but measures outside of the budget require 60 out of 100 Senate votes which will necessitate support from some Democrats.

-

His jawboning of US companies to keep production in the US could backfire leading to low US productivity. The track record of governments trying to direct companies is not great. But this will only become apparent over the long term and if production does remain in the US it will increasingly be dominated by robots anyway.

Assessing Trump

These risks are real but shouldn’t be exaggerated. In assessing Trump there are several key things investors need to allow for.

First, all new administrations make mistakes initially reflecting inexperience and the bureaucracy not yet in sync with the President. And with Trump and his team less experienced than most and the bureaucracy perhaps even less on side than normal, the mistakes are likely to be greater than normal. But as the process improves with the bureaucracy moving into line with the Trump administration, policy announcements should look smoother and more considered.

Second, he is not a traditional Republican president. Some of his policies are classic Republican – lower taxes, deregulation – but some borrow from the left – infrastructure spending or even old fashioned protectionism. Despite some comparisons to Ronald Reagan he lacks Reagan’s consistent ideology. He will follow his own course.

Third, his support base is middle America. Supporting them with jobs and higher wages is critical. Getting stuck in a trade war with China and Mexico that just pushes prices up at Walmart by 20% won’t go down well with his support base.

Fourth, he has a loud and more direct approach to communication – what some call a huge mega phone. And he has no constraint in using it against politicians or companies who get in his way. Related to this his open mouth approach is prone to reversal – think about his comments about locking Hilary Clinton up, border adjustment tax (initially “too complicated” but now working on it) and torture (initially supporting it and then leaving it to his Defence Secretary). We have to get used to a lot more noise coming out of Washington, but the key is that much of it will be just that: “noise”.

Fifth, he is a businessman who prides himself on his negotiating skills. So for example the imposition of a tariff on imports from China or Mexico may just be the opening gambit in a negotiation designed to extract a better trade deal for the US rather than necessarily being the final outcome.

Finally, his time to get his legislative agenda through Congress is limited. The President’s party normally loses control of it in the mid-term elections (as Obama did after his first two years) – so he doesn’t want to waste too much time.

On balance

Given all this I remain of the view that despite the rough start the pragmatic growth focussed Trump will ultimately dominate the populist Trump. But we have to allow that it will take a while for pro-growth policies to be legislated – eg, the President and Congress may not agree a tax reduction package until later this year – and that fears of trade war are likely to get worse before they get better as Trump embarks on a tough negotiating stance. This should ultimately be supportive of US/global growth but there will be volatility (and noise) along the way.

Implications for investment markets

After their large gains from around the US election, share markets, the US dollar and bond yields all entered 2017 with a degree of vulnerability. Shares, for example, had become technically overbought, and short term measures of investor sentiment had risen to levels of optimism that are often associated with a correction. See the next chart for US shares which tracks a measure of short term investor sentiment based on surveys of investor optimism and demand for option protection against the US share market.

Source: Bloomberg, AMP Capital

Since Trump’s election played a part in the rally, it was always likely that a period of uncertainty about what Trump would do – whether we get the pragmatist or the populist – could drive this, and this seems to be the case. This in fact is not out of line with the historical experience where US shares in the first February of new presidents have had an average decline of 4% since Hoover in 1929. Of course other factors played a role: with the Great Depression for Roosevelt; the start of the tech wreck for G W Bush; and the tail end of the GFC for Obama exaggerating the declines they saw. But the pattern of an initial period of uncertainty, often around communication mistakes, is apparent.

Source: Thomson Reuters, AMP Capital

However, despite the likelihood of a bout of short term market turbulence we see share markets trending higher over the next 6-12 months helped by okay valuations, continuing easy global monetary conditions, some acceleration in global growth, rising profits in both the US and Australia, and as Trump’s pro-growth policies start to impact.

A brief comment on border adjustment tax

Debate about a “border adjustment tax” in the US is heating up, but what is it? Basically many countries including Australia and Europe have a consumption tax – which only taxes goods and services consumed in the country. So imports are taxed and exports aren’t. The US has state based sales taxes but these are not the same as a consumption tax. In part to address the imbalance and at the same time lower America’s corporate tax rate from a globally high 35%, House Republicans have been working to move the US corporate tax system to only tax activity relating to goods and services consumed in the US. This would entail taxing imports and rebating tax on exports, ie, undertaking a “border adjustment”, just like when tourists show up at the airport when leaving Europe for a tax refund on goods they have bought there. Such an approach would make it harder for companies to lower their taxable income (via transfer pricing), redress the imbalance where the US does not have a consumption tax but other countries do, and because America imports more than it exports it would enable a lower corporate tax rate with talk of a 20% rate.

Trump initially rejected the idea as being “too complicated” but appears to have come round to it lately. However, it’s not clear Republican senators would support it and there is a long way to go. But if it does get up it would be a huge boost for US exporters (eg, Boeing) and a huge negative for importers (eg, Walmart) and would put significant upwards pressure on the $US which could then nullify the border adjustment. Of course it may also be subject to a World Trade Organisation challenge (although the US may argue most other countries do the same with their consumption taxes) and it would put significant pressure on other countries to move to the same system.

At the very least a 20% US corporate tax rate would only add to the pressure on Australia to lower its corporate tax rate.

Source: AMP Capital 02 Feb 2017

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

2017 – a list of lists regarding the macro investment outlook

Despite a terrible start to the year and a few political surprises along the way, 2016 saw good returns for diversified investors who held their nerve. Balanced super funds had returns around 7.5%, which is pretty good given inflation was just 1.5%. 2017 is commencing with less fear than seen a year ago but there is consternation regarding

Read More  Despite a terrible start to the year and a few political surprises along the way, 2016 saw good returns for diversified investors who held their nerve. Balanced super funds had returns around 7.5%, which is pretty good given inflation was just 1.5%. 2017 is commencing with less fear than seen a year ago but there is consternation regarding Donald Trump’s policies, political developments in Europe and the growth outlook. This note provides a summary of key insights on the global investment outlook and key issues around it in simple dot point form.

Despite a terrible start to the year and a few political surprises along the way, 2016 saw good returns for diversified investors who held their nerve. Balanced super funds had returns around 7.5%, which is pretty good given inflation was just 1.5%. 2017 is commencing with less fear than seen a year ago but there is consternation regarding Donald Trump’s policies, political developments in Europe and the growth outlook. This note provides a summary of key insights on the global investment outlook and key issues around it in simple dot point form.

Seven lessons from 2016

-

Global growth may be constrained – but it’s far stronger and more resilient than was feared at the start of 2016.

-

The US Federal Reserve is not stupid – it is not on “rate hike autopilot” and takes account of global conditions and the $US and the impact of both on the US.

-

China won’t tolerate a rapid slowing in economic growth – yes it wants to reform the supply side of its economy and slow down the growth of debt but it will not do so blindly.

-

Geopolitics is having a rising impact on investment markets – in part a populist backlash against establishment politics with implications for economic policy, eg, globalisation.

-

But, turn down the noise – fears that Brexit, Australia’s messy election, a Trump victory and an Italian “No” vote would lead to financial catastrophe proved ill-founded. Retreating to cash after these would have been costly.

-

The terror threat is alive and well but the impact on investment markets is limited.

-

Stick to an investment strategy – 2016 proved distracting for investors but they would have done okay provided they stuck to an investment strategy that prevented them from getting blown around by swings in market sentiment.

Key themes for 2017

-

Global growth of around 3.2% or just above, with the US around 2.5%, Europe and Japan lagging and China running around 6.5%. Australian growth of around 2.5%.

-

A gradual rise in underlying inflation, albeit from low levels.

-

Global monetary conditions remaining easy but less so, with gradual monetary tightening in the US and China offset by ongoing easing in Europe, Japan and Australia.

-

Reflecting this, global shares are likely to trend higher and we favour Europe and Japan over the US (which may be constrained after its 2016 outperformance and Fed hikes).

-

Australian shares are likely to have solid returns as resource sector profits surge following the rebound in bulk commodity prices, overall profits rise 10% and interest rates remain low.

-

Still low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds.

-

Commercial property and infrastructure are likely to continue benefitting from investors’ ongoing search for yield, but this demand will wane as bond yields trend higher.

-

Australian capital city residential property price gains are expected to slow to around 3-4%, as the heat comes out of the Sydney and Melbourne markets and rising supply hits.

-

Cash and bank deposit returns will remain poor.

-

The downtrend in the $A from 2011 is likely to continue as the interest rate differential in favour of Australia narrows and it undertakes its usual undershoot of fair value.

Key risks for 2017

-

President Trump could set off a global trade war and wider political tensions with China (eg, in the South China Sea).

-

US fiscal stimulus under Trump could overheat the US economy resulting in an aggressive Fed & a further rebound in the $US causing problems for emerging countries.

-

A further rapid rise in bond yields would be bad for shares and assets that have benefitted from the search for yield including real estate and infrastructure investments.

-

Success by populist parties in Europe could reignite Eurozone break up fears.

-

China could have its long feared hard landing.

-

Australia could be vulnerable as apartment supply surges and housing construction slows.

-

Factor X – there is always something from left field. Last year it was the rise of populism in some Anglo countries.

Five things to watch

-

President Trump – whether we get Trump the pragmatist or Trump the populist.

-

US inflation and the Fed – how quickly both move up.

-

Elections in the Netherlands in March, France in April/May, Germany around September and possibly in Italy.

-

Global business conditions indicators (PMIs).

-

Business confidence & non-mining investment in Australia.

Three reasons why global growth is likely to continue

-

We have not seen the excesses (massive debt growth, overinvestment, plunging spare capacity or excessive inflation) that normally precede recessions.

-

The US monetary tightening cycle is in its very early stages and global monetary conditions are still very easy.

-

Fiscal austerity has faded and we are seeing early signs of a shift from monetary easing (which arguably has become less potent) to fiscal stimulus.

Three reasons to expect Trump the pragmatist to ultimately take precedence

Donald Trump’s anti-establishment mandate, bellicose approach and inexperience will no doubt continue to create much uncertainty about his policies in the short term. His war with the media, issues around Russia and potential conflicts of interest add to the risks. However, there are reasons to expect that on the policy front pragmatism will ultimately prevail with the focus being on the growth boosting potential of tax cuts, infrastructure spending and deregulation:

-

Economic and political realities (including Congress) invariably take some of the edge off more radical policies once politicians attain power.

-

Trump has a focus on growth and jobs and won’t want to threaten this which suggests pragmatic policy outcomes.

-

As a businessman he is likely to ultimately seek win/win solutions with other countries (notably China) even though he may use a bellicose negotiating stance.

Three reasons why Chinese growth will likely come in around 6.5% and not much lower

-

Stimulus measures over the last two years highlight the government has no tolerance for a collapse in growth.

-

The services sector is taking over from manufacturing.

-

Deflation is receding as indicated by rising producer prices.

Three reasons why geopolitics is more important

-

The slow post GFC recovery, rising inequality in some countries and stress around immigration are leading to a backlash against establishment politicians.

-

The relative decline of the US is shifting us away from the unipolar world that dominated post the Cold War (where the US was the world’s cop) to a less stable multi-polar world (where skirmishes and proxy wars are more common). The symbiotic relationship between the US and China is fading.

-

The information revolution is enabling us to make our own reality, with the decline of traditional media in favour of online news sources that can be less reliable or self-selected. Conspiracy theories go mainstream!

Four reasons why the Eurozone won’t break up

Eurozone break up fears will again feature with elections in the Netherlands, France and Germany and maybe Italy. But there are three reasons why it won’t break up… well at least not yet:

-

Most of Europe does not have the problems with inequality that have helped drive Brexit and Trump.

-

Eurozone break up risk arguably peaked a few years ago when austerity and unemployment were at their peak.

-

Support for Eurosceptic parties has not picked up significantly since Brexit and Trump and support for the Euro in mainstream Europe remains high.

Five reasons why Australia won’t have a recession

-

Interest rates can still fall further if needed.

-

The drag on the economy from falling mining investment is fading and should bottom in the next year or so.

-

National income is rising thanks to rising commodity prices.

-

Sectors such as tourism and higher education (both helped by the lower $A) along with state capital spending should help offset the gap left by slowing housing investment

-

Stronger export volumes (from resource projects) will provide a partial offset to lower commodity prices.

Five reasons the RBA is more likely to cut than hike

-

The outlook for business investment is still weak.

-

To offset a slowing contribution to growth from housing.

-

The $A needs to fall further.

-

To offset the monetary tightening from bank mortgage rate hikes for existing home owners.

-

Inflation is likely to remain below target for longer.

Three reasons why the super cycle bond bull market from the early 1980s is likely over

-

Deflation is waning with commodity prices hitting bottom.

-

Global spare capacity is gradually being used up.

-

Bonds are over-loved having benefitted from a huge flow out of equities since the GFC.

Five reasons why shares are likely to provide decent returns by year end…

-

Shares are not overvalued against still low bond yields and interest rates.

-

A global recession looks a long way away.

-

A pick up in global growth should help profits.

-

Monetary conditions are still very easy and while the Fed will continue to tighten other central banks are still easing.

-

There is a lot of pessimism around.

…but three reasons to expect continued volatility

-

Much uncertainty remains in the short term around President Trump’s policies.

-

Geopolitical risks could flare up – particularly between the US and China and in Europe.

-

Shares are not dirt cheap anymore.

Nine things investors should remember

-

The power of compound returns – saving regularly in growth assets can grow wealth substantially over long periods. Using the “rule of 72” it will take 29 years to double an asset’s value if it returns 2.5% pa (ie 72/2.5) but only 9 years if the asset returns 8% pa.

-

The cycle lives on – markets cycle up and down and we need to allow for it and not get thrown off by rough patches.

-

Diversify – don’t put all your eggs in one basket.

-

Turn down the noise – this was a big one in 2016 where the noise around political events really just created distractions.

-

Starting point valuations matter – for example low bond yields will mean low medium term bond returns.

-

Remember that while shares can be volatile, the income stream from a diversified portfolio of shares is more stable over time and higher than the income from bank deposits.

-

Avoid the crowd – at extremes it’s invariably wrong.

-

Focus on investments providing sustainable and decent cash flows – not financial engineering.

-

Accept that it’s a low nominal return world – when inflation is 2% a 7.2% super return (the average for balanced growth super funds over the last three years) is pretty good.

Source: AMP Capital 25 Jan 2017

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Review of 2016, outlook for 2017 – looking better despite the political noise

US share market analyst Joe Granville once observed that “if it’s obvious, it’s obviously wrong”. 2016 was perhaps remarkable for the things that many thought were obvious at the start of the year but did not happen: the global economy did not see plunging growth and deflation; the Fed did not blindly raise interest

Read More2016 – a messy but okay year

US share market analyst Joe Granville once observed that “if it’s obvious, it’s obviously wrong”. 2016 was perhaps remarkable for the things that many thought were obvious at the start of the year but did not happen: the global economy did not see plunging growth and deflation; the Fed did not blindly raise interest rates; commodity prices did not continue to crash; the Brexit vote did not plunge the world into a growth slump; the election of Donald Trump did not cause a share market crash; China did not hard land (again); Europe did not break apart; tensions in the South China Sea did not bubble over into war; and the Australian property market did not collapse. What did happen was far more mundane:

-

The global economy continued to muddle along, at around 3% growth. The good news is that growth indicators stabilised and improved through the year helped in particular by stronger growth in the US after a slow start and a stabilisation in Chinese growth.

-

Fading deflation risks. While talk of deflation was all the rage early in the year this faded as commodity prices bottomed, spare capacity was gradually being used up and as the policy focus shifted from monetary to fiscal stimulus.

-

Rising commodity prices. An upswing in industrial commodity prices surprised many and was driven by a combination of better than feared demand and supply cuts.

-

Politics turned populist. The Brexit vote, the US election, the Australian election and some say the Italian referendum highlighted to varying degrees the rising support for populist solutions and a backlash against globalisation.

-

Another year of easy money. While growth fears and politics saw the Fed scale back its planned rate hikes, central banks in Europe & Japan remained in easing mode as did the People’s Bank of China during much of the year.

-

The great policy rotation. While monetary conditions remained ultra easy the realisation that monetary policy could only do so much combined with populist political pressures saw more talk of a shift towards fiscal stimulus. President elect Trump is at the pointy end of this move.

-

Low inflation saw more rate cuts in Australia and growth disappointed. Australian growth started off strong but weakened in the second half. Rebalancing is continuing, with NSW and Victoria continuing to do well, but a dip in inflation well below target saw the RBA continue cutting interest rates. Meanwhile, the risks continued to build around the Sydney and Melbourne housing markets.

While the macro environment turned out okay – the growth scare early in the year along with political events made for a constrained and at times interesting ride in investment markets.

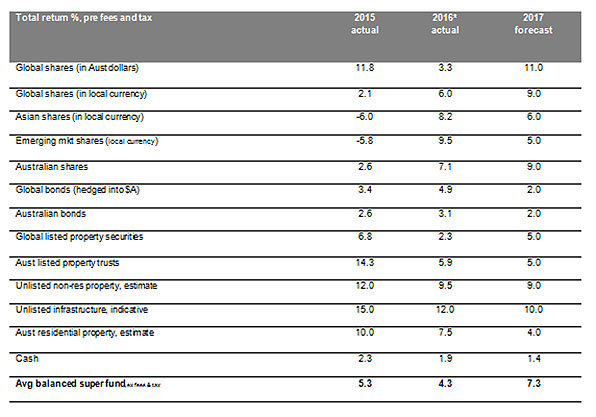

Investment returns for major asset classes

* Yr to date to Nov. Source: Thomson Reuters, Morningstar, REIA, AMP Capital

-

In contrast to 2015 that saw share markets start well and end badly, share markets started 2016 badly on growth and deflation fears before rebounding as such fears faded. The Brexit vote, the US election and the Italian referendum caused only short lived scares.

-

2016 saw a classic reversal of some of the relative share market performances that had been seen into 2015, with: US shares outperforming in developed markets as the Fed paused, the US earnings recession ended and investors anticipated stimulus under a Trump presidency; resources shares outperforming as commodity prices rebounded helping the Australian share market to perform relatively well; and emerging markets doing well led by Brazil.

-

After a huge rally in the first half of the year bonds then gave up their gains spurred along by anticipation of fiscal stimulus under Donald Trump. So bond returns were subdued.

-

Real estate investment trusts surged in the first half of the year, but fell as bond yields rose, constraining their returns

-

Unlisted commercial property and infrastructure continued to benefit as investors sought decent income yields.

-

Australian residential property returns were solid but slowed and remained concentrated in Sydney and Melbourne.

-

Cash rates and bank term deposit returns were poor reflecting record low RBA interest rates.

-

After several years of falls, the $A fell actually rose 3% as the Fed delayed and commodity prices rose.

-

Balanced superannuation funds returns were subdued, but better than cash and bank deposits.

2017 – looking better despite the noise

Of course those who foresaw the “financial crisis of 2016” will just roll their call into 2017! But there are good reasons to believe disaster will yet again be averted.

-

Leading growth indicators such as business conditions PMIs have reaccelerated after a 2015-16 soft patch and actually point to stronger growth.

Source: Bloomberg, IMF, AMP Capital

-

There is no sign of the sort of excesses that drive recessions & deep slumps in shares: there has been no major global bubble in real estate or business investment; inflation remains low; share markets are not unambiguously overvalued and global monetary conditions are easy.

-

While the Fed is likely to raise interest rates several times in 2017 this will likely be offset by fiscal stimulus from the Trump administration equal to around 1% of GDP. Rate hikes are likely to be limited to the extent that the rising $US is doing part of the Fed’s job.

-

Meanwhile monetary conditions will generally remain easy in the Eurozone and Japan with a further easing likely in Australia, albeit a tightening phase is possible in China.

Against this background:

-

Global growth is likely to move just above 3%, ranging from around 2% in advanced countries to around 6% in China.

-

Headline inflation is likely to continue to rise as commodity prices rise with core inflation rising more slowly.

-

The earnings recession looks to have ended – at least in the US & Australia – with solid earnings growth likely.

-

Bond yields have gone up too far too fast in the short term, but the trend is likely to be gradually up.

For Australia, the economy is likely to continue to rebalance away from mining investment and pick up again from its September quarter decline: the ramp up in resource export volumes has further to go; there is still a huge pipeline of housing activity yet to be completed; strengthening approvals point to stronger non-dwelling construction; the drag from mining investment is fading as it falls as a share of GDP and its likely to be close to a bottom next year; recent retail sales data have improved suggesting a consumer bounce back in the December quarter and the rebound in commodity prices tells us that the income recession in Australia is over. Expect Australian growth to be around 2.5% through 2017.

However, near term risks to Australian growth are on the downside, inflation is likely to remain below target for longer than the RBA is forecasting, the RBA is likely to need to offset increases in bank mortgage rates and the $A remains too high. So we expect another rate cut in the first half of next year taking the cash rate to 1.25%. A rate hike is a long way off.

Implications for investors?

The combination of some acceleration in global growth, rising profits and still easy money at a time when investors are highly sceptical (and ever fearful of the next GFC) should be positive for growth assets in 2017:

-

Global shares are likely to trend higher and we favour Europe (which is very cheap and likely to climb a wall of Eurozone break-up worries) and Japan (which will benefit from the lower Yen) over the US (which may be constrained after its 2016 outperformance and Fed rate hikes).

-

Emerging markets may underperform if the $US continues to rise on Fed hikes but for now are looking attractive if as we expect the rise in the $US takes a break early in 2017.

-

Australian shares are likely to have solid returns as resource sector profits surge following the rebound in bulk commodity prices, overall profits rise 10% and interest rates remain low. Expect the ASX 200 to reach 5800 by end 2017. In terms of sectors favour resources, retailers, and banks.

-

Commodity prices are at risk of a short term pause/pull back but should remain well up from their 2015-16 lows.

-

Still low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds.

-

Commercial property and infrastructure are likely to continue benefitting from the ongoing search by investors for yield.

-

National capital city residential property price gains are expected to slow to around 3-4%, as the heat comes out of the Sydney and Melbourne markets and rising supply hits.

-

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

-

The downtrend in the $A is likely to continue as the interest rate differential in favour of Australia narrows and it undertakes its usual undershoot of fair value. Expect a fall below $US0.70 but little change versus the Yen and Euro.

What to watch?

The main things to keep an eye on in 2017 are:

-

US economic policy under President Trump – in particular whether the focus is on fiscal stimulus and deregulation as opposed to starting a trade war with China;

-

How aggressively the Fed raises rates – faster inflation could speed it up putting more upwards pressure on the $US;

-

A rapid rise in bond yields – this would be bad for shares and growth assets but a gradual rise would be okay;

-

Elections in the Netherlands, France, Germany and maybe Italy which could reignite Eurozone break-up fears if anti-Euro populists win (which I doubt they will);

-

Whether China continues to avoid a hard landing;

-

Whether non-mining investment picks up in Australia – a failure to do so could see aggressive RBA easing – and how a surge in apartment supply impacts property prices; and

-

Ongoing geopolitical flare ups, eg in the South China Sea.

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Brexit, Trump…Itexit, Le Pen, Eurozone break-up…or is Europe different? Implications for investors

After the recent experience with the Brexit vote in the UK and election of Donald Trump as President of the US which are indicative of a nationalist backlash against the pro-globalisation establishment, there is a fear that Europe will go the same way with nationalist forces in Italy, Austria, France, Germany, etc, triggering a break-up of the Eurozone. Of course

Read MoreIntroduction

After the recent experience with the Brexit vote in the UK and election of Donald Trump as President of the US which are indicative of a nationalist backlash against the pro-globalisation establishment, there is a fear that Europe will go the same way with nationalist forces in Italy, Austria, France, Germany, etc, triggering a break-up of the Eurozone. Of course a break-up of the Eurozone has the potential to be a more traumatic event than the UK leaving the European Union or the change of Presidency in the US. This is because currencies would have to be re-denominated and borrowing costs pushed up in more heavily indebted peripheral Eurozone countries to reflect a likely sharp decline in the value of their new currencies, which would likely trigger a recession in them. At the same time the weakening of key European export markets would be bad for Germany. The threat of which could cause a return to the sort of global financial volatility we have seen during various flare-ups of the Eurozone public debt crisis since 2010, most recently in mid-2015 with worries about Greece (remember Grexit !)

Some see a Eurozone break-up as inevitable, but is it really?

Event risk in Europe to keep break up risk in focus

The next 12 months are scattered with numerous events in the Eurozone that risk adding to investor concerns about a break-up: the Austrian presidential election re-run and Italian Senate referendum both to occur this coming Sunday; parliamentary elections in the Netherlands in March 2017; the presidential election in France in late April/early May and parliamentary elections in June; German general elections around September; and of course ongoing risks regarding Greece.

Opinion polls in Austria are pointing to the election of the populist right wing candidate Norbert Hofer and Italian opinion polls are pointing to a “No” vote in the Senate referendum (designed to reduce the power of the Senate and make Italy more governable) which would thwart PM Matteo Renzi’s reform agenda which in turn could see him resign with fears that this will lead to an early election with the Euro-sceptic Five Star Movement (5SM) winning, calling a referendum on Italy’s membership of the Eurozone which would then see Italy move to leave (Itexit). The political uncertainty that could be unleashed by an Italian “No” vote also risks throwing the recapitalisation of several Italian banks into turmoil which could threaten already weak economic growth further boosting support for 5SM. Reflecting all this Italian bond yields have risen from 1.1% to 2% over the last six months compared to a rise from -0.09% to 0.2% in Germany. In other words investors are demanding a higher premium again to lend to Italy for fear its Euro debt will be redenominated into lower value Liras.

However, a lot of water would have to pass under the bridge for Austria or Italy to leave the Eurozone. Firstly, I guess if after Brexit and Trump you no longer trust opinion polls you could argue that there is nothing to worry about as Nofer will lose the Austrian election and the “Yes” vote will win in Italy! (Actually the polls did an ok job on Brexit and Trump – it was the betting markets that were way out!) More fundamentally though, after marginally losing the first Austrian presidential election in May, Hofer has backed down on most of his anti-Euro rhetoric (no doubt in order to win the election) and so if he wins it wouldn’t mean an Ausexit (Austrian exit from the Euro) any time soon. Italy is more significant though but the Senate referendum’s failure would just mean messy politics as normal in Italy (either under Renzi or an alternative). However, it’s unlikely there will be an election before the due date in 2018, and even if there was it’s not clear that 5SM would win. And even if 5SM were to win and call a referendum on Italy’s membership of the Euro (which would first require a constitutional change), a majority of Italians support staying in the Euro.

Europe could be different

Looking at the big picture there are several reasons for thinking that Europe might be different – that a populist driven break-up won’t happen. First, Europe does not have the same issues with inequality that has driven the “leftist” backlash in the UK and US, which has helped fuel nationalist anger. It never really had the lurch to laissez-faire economics that Anglo countries saw in the 1980s and so has maintained a large social welfare state. This has helped redistribute the benefits of globalisation such that inequality has remained well below US and UK levels, as can be seen in the next chart which shows Gini coefficients (a measure of income inequality) are below average in Europe.

Source: OECD, AMP Capital

Second, Eurozone break-up risk is nothing new and arguably peaked just after the high point of the Eurozone debt crisis (which at its core was all about break-up risk) a few years ago when austerity and unemployment were at their peak. Now austerity has largely ended and unemployment is falling.

Third, despite the media excitement (made worse in Anglo countries who would love to see the Eurozone collapse) the increase in support for Euro-sceptic populists following Brexit and Trump has not really been overwhelming (next chart).

Source: Bloomberg (from various polls), AMP Capital

-

Following Brexit, Spain has seen reduced support for far left Podemos in favour of the governing People’s Party.

-

Support for Le Pen and the National Front in France is stuck around 30% and has actually been in decline since 2013. She will likely win the first round of the presidential election in April (which will involve multiple candidates) but lose the second round run-off between the top two particularly with a strong centre-right candidate in the form of François Fillon seeing support of around 65-70%.

-

The Dutch Eurosceptic Party for Freedom has seen support decline this year – perhaps as the immigration crisis has faded – such that it may only get 10% support in March.

-

The Five Star Movement in Italy looks to have peaked in the polls, and polls less than the governing party.

-

Alternative for Deutschland only gets about 15% support, and Angela Merkel’s decision to run for a fourth term adds to confidence a centrist government will remain in Germany

Fourth, support in mainland Europe for the Eurozone remains high. In the Netherlands its 75%, in France it’s around 67% and in Italy it’s around 55%. Basically the populists have to ditch anti-Euro policies if they wish to govern. Just look at Syriza in Greece which has gone from being a far left Euro-sceptic party to just another European centrist political party.

The commitment of continental Europeans to Europe and the Euro is arguably more about politics than economics. It’s rooted in being part of a stronger whole and a desire to avoid a return to the conflict that prevailed up until WW2. In part reflecting this, mainland Europeans are far more likely to see themselves as European than the British ever did. See next chart.

Source: Eurobarometer, AMP Capital

Pressure points

Perhaps the two main pressure points in Europe beyond slow economic growth are the migration crisis and fiscal austerity. But the migration crisis is abating as sea arrivals have collapsed from over 200,000 a month in October 2015 to below 3000 recently with mainstream governments now taking a tougher line on it. Meanwhile, fiscal austerity in Europe largely ended in 2013 (see the next chart) with the European Commission now recommending that member countries with fiscal space adopt a more expansionary fiscal stance.

Source: IMF Fiscal Monitor, AMP Capital

Implications for investors

There are several implications for investors. First, various events – the upcoming Austrian election & the Italian referendum and 2017 elections in the Netherlands, France and Germany – will no doubt keep Eurozone break-up fears alive causing periodic short term investment market volatility.

Second, a “No” vote in Italy with risks for Italian banks along with political risk through next year will add to pressure on the European Central Bank to extend its quantitative easing program (and possibly step up Italian bond purchases). Which in turn will maintain downwards pressure on the Euro.

Finally, if we are right and the Eurozone continues to hang together then bouts of financial turmoil triggered by break-up fears are buying opportunities – just as we have seen since the Eurozone debt crisis began in 2010.

More broadly, after their post Trump rally shares have become overbought and vulnerable to various events coming up over the next few weeks (Italian referendum, ECB and Fed meetings), but after a pause shares are likely to resume their rally into year-end helped by reasonable valuations, continuing easy global monetary conditions, the prospect of fiscal stimulus in the US, a shift from falling to rising profits and the usual “Santa Claus” rally that kicks in around mid-December.

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Source: AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Brexit, Trump…Itexit, Le Pen, Eurozone break-up…or is Europe different? Implications for investors

After the recent experience with the Brexit vote in the UK and election of Donald Trump as President of the US which are indicative of a nationalist backlash against the pro-globalisation establishment, there is a fear that Europe will go the same way with nationalist forces in Italy, Austria, France, Germany, etc, triggering a break-up of the Eurozone. Of course

Read MoreIntroduction

After the recent experience with the Brexit vote in the UK and election of Donald Trump as President of the US which are indicative of a nationalist backlash against the pro-globalisation establishment, there is a fear that Europe will go the same way with nationalist forces in Italy, Austria, France, Germany, etc, triggering a break-up of the Eurozone. Of course a break-up of the Eurozone has the potential to be a more traumatic event than the UK leaving the European Union or the change of Presidency in the US. This is because currencies would have to be re-denominated and borrowing costs pushed up in more heavily indebted peripheral Eurozone countries to reflect a likely sharp decline in the value of their new currencies, which would likely trigger a recession in them. At the same time the weakening of key European export markets would be bad for Germany. The threat of which could cause a return to the sort of global financial volatility we have seen during various flare-ups of the Eurozone public debt crisis since 2010, most recently in mid-2015 with worries about Greece (remember Grexit !)

Some see a Eurozone break-up as inevitable, but is it really?

Event risk in Europe to keep break up risk in focus

The next 12 months are scattered with numerous events in the Eurozone that risk adding to investor concerns about a break-up: the Austrian presidential election re-run and Italian Senate referendum both to occur this coming Sunday; parliamentary elections in the Netherlands in March 2017; the presidential election in France in late April/early May and parliamentary elections in June; German general elections around September; and of course ongoing risks regarding Greece.

Opinion polls in Austria are pointing to the election of the populist right wing candidate Norbert Hofer and Italian opinion polls are pointing to a “No” vote in the Senate referendum (designed to reduce the power of the Senate and make Italy more governable) which would thwart PM Matteo Renzi’s reform agenda which in turn could see him resign with fears that this will lead to an early election with the Euro-sceptic Five Star Movement (5SM) winning, calling a referendum on Italy’s membership of the Eurozone which would then see Italy move to leave (Itexit). The political uncertainty that could be unleashed by an Italian “No” vote also risks throwing the recapitalisation of several Italian banks into turmoil which could threaten already weak economic growth further boosting support for 5SM. Reflecting all this Italian bond yields have risen from 1.1% to 2% over the last six months compared to a rise from -0.09% to 0.2% in Germany. In other words investors are demanding a higher premium again to lend to Italy for fear its Euro debt will be redenominated into lower value Liras.

However, a lot of water would have to pass under the bridge for Austria or Italy to leave the Eurozone. Firstly, I guess if after Brexit and Trump you no longer trust opinion polls you could argue that there is nothing to worry about as Nofer will lose the Austrian election and the “Yes” vote will win in Italy! (Actually the polls did an ok job on Brexit and Trump – it was the betting markets that were way out!) More fundamentally though, after marginally losing the first Austrian presidential election in May, Hofer has backed down on most of his anti-Euro rhetoric (no doubt in order to win the election) and so if he wins it wouldn’t mean an Ausexit (Austrian exit from the Euro) any time soon. Italy is more significant though but the Senate referendum’s failure would just mean messy politics as normal in Italy (either under Renzi or an alternative). However, it’s unlikely there will be an election before the due date in 2018, and even if there was it’s not clear that 5SM would win. And even if 5SM were to win and call a referendum on Italy’s membership of the Euro (which would first require a constitutional change), a majority of Italians support staying in the Euro.

Europe could be different

Looking at the big picture there are several reasons for thinking that Europe might be different – that a populist driven break-up won’t happen. First, Europe does not have the same issues with inequality that has driven the “leftist” backlash in the UK and US, which has helped fuel nationalist anger. It never really had the lurch to laissez-faire economics that Anglo countries saw in the 1980s and so has maintained a large social welfare state. This has helped redistribute the benefits of globalisation such that inequality has remained well below US and UK levels, as can be seen in the next chart which shows Gini coefficients (a measure of income inequality) are below average in Europe.

Source: OECD, AMP Capital

Second, Eurozone break-up risk is nothing new and arguably peaked just after the high point of the Eurozone debt crisis (which at its core was all about break-up risk) a few years ago when austerity and unemployment were at their peak. Now austerity has largely ended and unemployment is falling.

Third, despite the media excitement (made worse in Anglo countries who would love to see the Eurozone collapse) the increase in support for Euro-sceptic populists following Brexit and Trump has not really been overwhelming (next chart).

Source: Bloomberg (from various polls), AMP Capital

-

Following Brexit, Spain has seen reduced support for far left Podemos in favour of the governing People’s Party.

-

Support for Le Pen and the National Front in France is stuck around 30% and has actually been in decline since 2013. She will likely win the first round of the presidential election in April (which will involve multiple candidates) but lose the second round run-off between the top two particularly with a strong centre-right candidate in the form of François Fillon seeing support of around 65-70%.

-

The Dutch Eurosceptic Party for Freedom has seen support decline this year – perhaps as the immigration crisis has faded – such that it may only get 10% support in March.

-

The Five Star Movement in Italy looks to have peaked in the polls, and polls less than the governing party.

-

Alternative for Deutschland only gets about 15% support, and Angela Merkel’s decision to run for a fourth term adds to confidence a centrist government will remain in Germany

Fourth, support in mainland Europe for the Eurozone remains high. In the Netherlands its 75%, in France it’s around 67% and in Italy it’s around 55%. Basically the populists have to ditch anti-Euro policies if they wish to govern. Just look at Syriza in Greece which has gone from being a far left Euro-sceptic party to just another European centrist political party.

The commitment of continental Europeans to Europe and the Euro is arguably more about politics than economics. It’s rooted in being part of a stronger whole and a desire to avoid a return to the conflict that prevailed up until WW2. In part reflecting this, mainland Europeans are far more likely to see themselves as European than the British ever did. See next chart.

Source: Eurobarometer, AMP Capital

Pressure points

Perhaps the two main pressure points in Europe beyond slow economic growth are the migration crisis and fiscal austerity. But the migration crisis is abating as sea arrivals have collapsed from over 200,000 a month in October 2015 to below 3000 recently with mainstream governments now taking a tougher line on it. Meanwhile, fiscal austerity in Europe largely ended in 2013 (see the next chart) with the European Commission now recommending that member countries with fiscal space adopt a more expansionary fiscal stance.

Source: IMF Fiscal Monitor, AMP Capital

Implications for investors

There are several implications for investors. First, various events – the upcoming Austrian election & the Italian referendum and 2017 elections in the Netherlands, France and Germany – will no doubt keep Eurozone break-up fears alive causing periodic short term investment market volatility.

Second, a “No” vote in Italy with risks for Italian banks along with political risk through next year will add to pressure on the European Central Bank to extend its quantitative easing program (and possibly step up Italian bond purchases). Which in turn will maintain downwards pressure on the Euro.

Finally, if we are right and the Eurozone continues to hang together then bouts of financial turmoil triggered by break-up fears are buying opportunities – just as we have seen since the Eurozone debt crisis began in 2010.

More broadly, after their post Trump rally shares have become overbought and vulnerable to various events coming up over the next few weeks (Italian referendum, ECB and Fed meetings), but after a pause shares are likely to resume their rally into year-end helped by reasonable valuations, continuing easy global monetary conditions, the prospect of fiscal stimulus in the US, a shift from falling to rising profits and the usual “Santa Claus” rally that kicks in around mid-December.

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Source: AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.