Provision Newsletter

How global trends are creating infrastructure opportunities

Infrastructure investing is changing fast as evolving global trends throw up new opportunities.

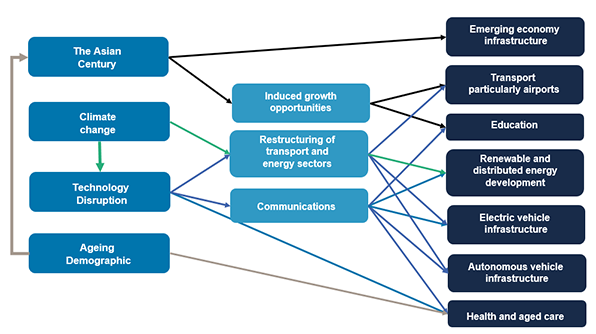

The rise of emerging Asian economies, climate change, technological disruption and the ageing demographic are transforming the demand for essential facilities across the developed world and beyond.

This is creating exciting investment opportunities for infrastructure investors who are examining this expanding asset class to capture global economic

Read MoreInfrastructure investing is changing fast as evolving global trends throw up new opportunities.

The rise of emerging Asian economies, climate change, technological disruption and the ageing demographic are transforming the demand for essential facilities across the developed world and beyond.

This is creating exciting investment opportunities for infrastructure investors who are examining this expanding asset class to capture global economic growth.

Source: AMP Capital

The Asian Century

The Chinese middle class has expanded enormously in recent years; from just 4% of its population in 2000, it is expected to reach 75% by 2022 according to McKinsey. Similar trends are becoming evident in India and south-east Asian economies. According to PwC, six of the world’s seven largest economies in 2050 will be current emerging economies; three of the top four being in Asia.

This is already fueling the infrastructure needs of those societies, as evidenced by the Chinese government’s One Belt One Road initiative. Fast rail links, the Hong Kong-Zhuhai-Macau Bridge and upgraded port facilities are all signs of this.

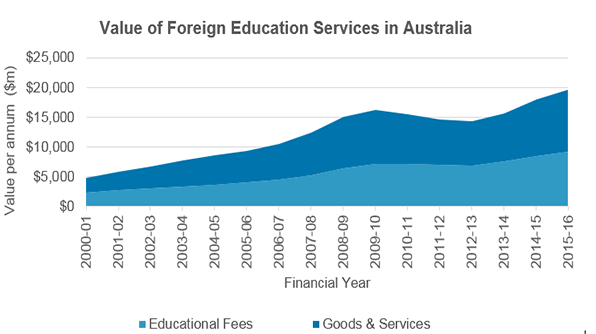

This trend is also impacting developed economies as the Asian middle class spends its new wealth in western countries. A university education in an English-speaking developed country is highly regarded across Asia. Education is now Australia’s largest service export.

This influx of international students is increasing the need for student accommodation attached to leading universities in countries such as Australia. This market expects a higher quality standard than traditional student housing, but its enhanced ability to pay gives rise to long-term high-yield investments that provide protection against inflation.

Source:ABS 5368.0.55.003

The emerging Asian middle class is also spending its new-found wealth on overseas travel. Long-haul air travel in the Asia Pacific region is forecast to grow in excess of 6% per year over the next 20 years.

Australian international airports have taken advantage of this, achieving some of the highest EBITDA growth amongst developed economy airports. A lack of spare capacity and technological improvements that enable more long-haul direct flights are boosting demand for new infrastructure projects to support this growing demand.

Climate change

The 2015 Paris Climate Change Agreement committed countries to take measures that would limit global warming to 2 degrees Celsius. This promise and the immediate impact of pollution are leading to the restructuring of transport and energy sectors.

Road congestion and pollution are leading to electric vehicles, greater experimentation with road charging, high-speed rail links and the expansion of mass transit networks in large urban areas. Such developments require large-scale construction projects and/or the handling of large volumes of data.

Climate change has also led governments to adjust the incentives that apply to energy supply in favour of renewables at the expense of fossil fuels. The profusion of wind, solar, hydro and tidal projects is well-established, however these are likely to continue to expand as their historic cost disadvantage continues to diminish.

Climate change also represents a challenge for the management and distribution of scarce urban water resources, in which private sector capital may well have a role to play.

Disruptive technology on a micro level is leading to energy cost savings for households when rooftop solar panels are integrated with advanced battery technology and connected to the electricity grid. Individual households have achieved cost savings in excess of 80% of their annual electricity bills through exploiting this technology.

Technology costs are expected to continue to fall, making such systems increasingly viable for the typical home owner. Furthermore, integration with network operations can improve grid productivity and also opens up an alternative power generation opportunity for infrastructure investors.

Technological disruption

Technological disruption is initiating a fourth industrial revolution as devices become automated and connected.

The decentralisation of work, energy and service provision is leading to more home working, energy self-sufficiency and local/home delivery. However these trends require ongoing investment in the data and logistical infrastructure required to support these lifestyle shifts.

Hybrid and electric cars and delivery trucks are already becoming a common sight across developed countries. Electric vehicles will be cheaper for consumers and permit the decarbonising of the transport sector.

Looking further ahead, automated vehicles (which will be overwhelmingly electrically-powered) will eventually deliver a more flexible alternative to conventional public transport methods and private car ownership.

However this will depend upon massive infrastructure capex to support the power and data transmission that will be required for the safe and reliable use of road space.

Ageing Demographic

Global fertility rates have halved since 1955 as much of the world has industrialised and life expectancy has risen in developing countries. However the demographic deficit is impacting low-nominal growth developed countries such as Japan and Italy as well as Russia and China. The size of Japan’s workforce has been declining since 1994 as demographics meet a cultural hesitation towards immigration.

This trend is leading to greater health spending; in the UK some 40% of the state-financed National Health Service is spent on the over-65s, a proportion that will continue to rise. Longer-term aged care facilities will also continue to see increasing demand.

These trends will lead to ongoing infrastructure capex as new facilities are established by both public and private sector providers.

Conclusions

A broad range of high-growth infrastructure investments will be generated by these major global structural themes.

Opportunities are most likely to arise in the transport, energy, data/communications and healthcare sectors.

While some of these opportunities, such as airports, will be quite familiar, others will be new, including disruptive technologies or those found in emerging economies. Sovereign and governance risks in these economies will require careful management and the selection of local partners.

These emerging opportunities will provide infrastructure investors with potentially higher returns (and potentially higher risks) which will complement conventional infrastructure investments. Success will depend upon good project selection and high levels of positive control to allow active ‘private equity-style’ asset management of investments.

The blending of higher return “new infrastructure” and traditional infrastructure will allow portfolio managers the ability to construct portfolios with a wide range of risk and return characteristics.

Source: AMP Capital 13 June 2018

Author: John Julian, Portfolio Manager, Core Infrastructure Fund

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Investors win from commodities cash flow boom

Dermot Ryan, Portfolio Manager, Australian Equites, AMP Capital

Resource companies are enjoying a resurgence in profits based on higher commodity prices and lower unit costs.

Now many of you might think, “well we’ve had booms before.” The big difference this time is that there is still a strong focus on reducing the price of production, even as prices for raw commodities

Read MoreDermot Ryan, Portfolio Manager, Australian Equites, AMP Capital

Resource companies are enjoying a resurgence in profits based on higher commodity prices and lower unit costs.

Now many of you might think, “well we’ve had booms before.” The big difference this time is that there is still a strong focus on reducing the price of production, even as prices for raw commodities continues to increase.

In the mining boom pre-Global Financial Crisis (GFC) we saw a sharp run up in commodity prices, and companies scrambling over one another to get mines built as quick as possible – irrespective of costs. This led to greenfield expansion and large amounts of money being spent on labour, machinery and procurement and many of these didn’t get a good cost outcome.

Now, I think we are in one of the best periods for franked returns in the mining industry since the that last boom.

It is refreshing to see, in so many cases, mining companies returning money to investors through dividends and buybacks, rather than just being on a mad rush for growth.

Economic Growth

Global economic growth is running hot. In the US, business confidence and employment growth have been rising, and in much of Europe the recovery is underway.

From China, the world’s biggest commodities consumer, we are seeing a lot of demand for seaborne high-grade commodities, and they are also looking to improve their air quality and the environment, which means there may well be a substitution of lower grade Chinese raw materials for higher grade imports.

I think there are interesting opportunities across areas such as energy, iron ore, copper, and also specifically commodities related to electric vehicles. Lithium producers are the biggest winners from this, and there is also strong demand for cobalt and graphite.

As we go through this point in the cycle where demand is still high and interest rates haven’t yet risen there is an opportunity for companies that have de-geared their balance sheets to use some of that capital to invest back into their mines.

Mining expansion rarely comes cheap and the Reserve Bank of Australia has kept interest rates on hold for 21 months now. AMP Capital does not expect a rate rise until 2020. However, should the US Federal reserve raise rates quickly there could be risks for commodity prices and Asia demand.

Mining stock values

Valuations are still quite reasonable in the mining space as well because people want to see how sustainable commodity prices are at this level. It wasn’t that long ago after all, that larger companies found themselves too heavily in debt and struggling to refinance during the GFC.

Revenue & Earnings for the Australian Metals and Mining industry group

* Forecast estimates only for 2018 and 2019. Actual future results could differ materially from any forecasts, estimates, or opinions.

Source: Factset Industry Consensus Estimates

The winners are those who can add incremental production to existing plants and reduce their unit costs per commodity and come down the cost curve. This particularly favors companies with expandable tier one assets.

Now, we seem to be in a more considered period where most moving factors point towards better returns at any given commodity prices. This is really encouraging for Australian investors.

Companies too are much more focused on capital allocation and returning cash to shareholders. These periods of high dividends in deeply cyclical sectors like mining don’t last forever but can be enjoyed by investors in the current market.

Source: AMP Capital 13 June 2018

Author: Dermot Ryan, Portfolio Manager, Australian Equites, AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

An update on Australian property prices

Driven by falling markets in Sydney and Melbourne, national house prices fell 0.1% in May, according to figures from property analytics group Core Logic. For the year from 31 May 2017 to 31 May 2018, prices were down 0.4% marking the first annual fall since October 20121.

But AMP Capital’s Head of Investment Strategy and Economics and Chief Economist Dr

Read MoreDriven by falling markets in Sydney and Melbourne, national house prices fell 0.1% in May, according to figures from property analytics group Core Logic. For the year from 31 May 2017 to 31 May 2018, prices were down 0.4% marking the first annual fall since October 20121.

But AMP Capital’s Head of Investment Strategy and Economics and Chief Economist Dr Shane Oliver says despite the falls, talk of a property market crash is overdone.

Sydney and Melbourne

Prices in Sydney fell 0.2% in May, while Melbourne prices fell 0.5%. In Sydney, the median house price is now $871,454 while in Melbourne it sits at $717,0202.

And depending on whether you’re a buyer or seller in those market, there’s more good or bad news to come.

“We expect prices in Sydney and Melbourne to fall another 4% or so this year, another 5% next year and to still be falling in 2020. Overall, Sydney and Melbourne are likely to see a top-to-bottom fall of around 15% spread out to 2020,” Shane says.

But in the other capital cities, where the housing markets haven’t boomed in recent years to the same extent as Sydney or Melbourne, the forecast is different.

Perth, Darwin and Canberra

Prices in Perth and Canberra were both down 0.1% in May, while Darwin prices were down 0.2%3.

However, all three markets are up for the quarter, and Shane says that prices in Perth and Darwin look to be at or close to bottoming, while Canberra is likely to see moderate price growth in the months to come.

Hobart

Still the star performer, Hobart property continued its upwards surge in May, rising another 0.8%. Prices there are up 12.7% for the year from 31 May 2017 to 31 May 20184.

“The Hobart market remains very strong and the boom in Hobart is likely to continue for a while yet,” Shane says.

Brisbane and Adelaide

In Brisbane property prices rose 0.2% in May, while in Adelaide they performed even better, up 0.5%, with Shane forecasting more moderate price growth to come for both of these cities5.

Regional areas v capital cities

Taken as a whole, the combined capital cities markets fell 0.2% in May, but regional locations are performing better – when combined, regional markets saw prices rise by 0.2% in May, with Geelong and Ballarat in Victoria, the Southern Highlands, Newcastle and Coffs

Harbour in NSW and Queensland’s Sunshine Coast among the best performers6.

“Home prices in regional centres are likely to hold up better with continuing modest growth as, generally speaking, they haven’t had the same boom as Sydney and Melbourne and so offer much better value and much higher rental yields,” Shane says.

What’s driving the property market?

Shane says that a combination of factors is behind the falling markets, including:

-

Investors, people looking for interest-only loans and borrowers with constrained incomes and high expenses finding it more difficult to get finance, as banks have tightened their lending criteria due to pressure from regulators,

-

Tougher restrictions being imposed on foreign buyers by state and federal governments,

-

Rising levels of housing supply, and

-

Buyers with more realistic price expectations.

Shane says that interest rates are likely to remain at their current levels until 2020 but adds that with “home price weakness at levels where the Reserve Bank of Australia started cutting rates in 2008 and 2011, we can’t rule out the next move in rates being a cut rather than a hike”.

He says that unless interest rates or unemployment unexpectedly skyrocket talk of a property market crash has been overdone.

1-6 Core Logic, Hedonic Home Value Index, May 2018.

Source: AMP Capital 13 June 2018

Important information

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.

Has the housing bubble burst?

Driven by falling markets in Sydney and Melbourne, national house prices fell 0.1% in May, according to figures from property analytics group Core Logic. For the year from 31 May 2017 to 31 May 2018, prices were down 0.4% marking the first annual fall since October 20121.

But AMP Capital’s Head of Investment Strategy and Economics and Chief Economist Dr Shane Oliver

Read MoreDriven by falling markets in Sydney and Melbourne, national house prices fell 0.1% in May, according to figures from property analytics group Core Logic. For the year from 31 May 2017 to 31 May 2018, prices were down 0.4% marking the first annual fall since October 20121.

But AMP Capital’s Head of Investment Strategy and Economics and Chief Economist Dr Shane Oliver says despite the falls, talk of a property market crash is overdone.

Sydney and Melbourne

Prices in Sydney fell 0.2% in May, while Melbourne prices fell 0.5%. In Sydney, the median house price is now $871,454 while in Melbourne it sits at $717,0202.

And depending on whether you’re a buyer or seller in those market, there’s more good or bad news to come.

“We expect prices in Sydney and Melbourne to fall another 4% or so this year, another 5% next year and to still be falling in 2020. Overall, Sydney and Melbourne are likely to see a top-to-bottom fall of around 15% spread out to 2020,” Shane says.

But in the other capital cities, where the housing markets haven’t boomed in recent years to the same extent as Sydney or Melbourne, the forecast is different.

Perth, Darwin and Canberra

Prices in Perth and Canberra were both down 0.1% in May, while Darwin prices were down 0.2%3.

However, all three markets are up for the quarter, and Shane says that prices in Perth and Darwin look to be at or close to bottoming, while Canberra is likely to see moderate price growth in the months to come.

Hobart

Still the star performer, Hobart property continued its upwards surge in May, rising another 0.8%. Prices there are up 12.7% for the year from 31 May 2017 to 31 May 20184.

“The Hobart market remains very strong and the boom in Hobart is likely to continue for a while yet,” Shane says.

Brisbane and Adelaide

In Brisbane property prices rose 0.2% in May, while in Adelaide they performed even better, up 0.5%, with Shane forecasting more moderate price growth to come for both of these cities5.

Regional areas v capital cities

Taken as a whole, the combined capital cities markets fell 0.2% in May, but regional locations are performing better – when combined, regional markets saw prices rise by 0.2% in May, with Geelong and Ballarat in Victoria, the Southern Highlands, Newcastle and Coffs Harbour in NSW and Queensland’s Sunshine Coast among the best performers6.

“Home prices in regional centres are likely to hold up better with continuing modest growth as, generally speaking, they haven’t had the same boom as Sydney and Melbourne and so offer much better value and much higher rental yields,” Shane says.

What’s driving the property market?

Shane says that a combination of factors is behind the falling markets, including:

-

Investors, people looking for interest-only loans and borrowers with constrained incomes and high expenses finding it more difficult to get finance, as banks have tightened their lending criteria due to pressure from regulators,

-

Tougher restrictions being imposed on foreign buyers by state and federal governments,

-

Rising levels of housing supply, and

-

Buyers with more realistic price expectations.

Shane says that interest rates are likely to remain at their current levels until 2020 but adds that with “home price weakness at levels where the Reserve Bank of Australia started cutting rates in 2008 and 2011, we can’t rule out the next move in rates being a cut rather than a hike”.

He says that unless interest rates or unemployment unexpectedly skyrocket talk of a property market crash has been overdone.

Please contact us on |PHONE|if you seek further assistance .

1-6 Core Logic, Hedonic Home Value Index, May 2018.

Monetary Policy Decision – Statement by Philip Lowe, RBA Governor, June 2018

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and

Read MoreAt its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Financial markets have been affected by political developments in the eurozone, particularly in Italy. There are also concerns about the direction of international trade policy in the United States and economic developments in a few emerging market economies. Long-term bond yields in most major economies have declined recently and there has been some widening of corporate credit spreads. Overall, though, financial conditions remain expansionary. Conditions in US dollar short-term money markets have eased recently, although they are tighter than earlier in the year, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. The higher rates in the United States have flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased over recent months, as have the prices of some base metals. Australia’s terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The recent data on the Australian economy have been consistent with the Bank’s central forecast for GDP growth to pick up, to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has been little changed at around 5½ per cent for much of the past year. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a gradual reduction in the unemployment rate expected. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. Housing credit growth has slowed over the past year, especially to investors. APRA’s supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high. While there may be some further tightening of lending standards, the average mortgage interest rate on outstanding loans is continuing to decline.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Source: Reserve Bank of Australia, June 5th, 2018

Enquiries

Media and Communications

Secretary’s Department

Reserve Bank of Australia

SYDNEY

Phone: +61 2 9551 9720

Fax: +61 2 9551 8033

Email: rbainfo@rba.gov.au

China’s economy is pretty stable – but what about high debt levels and other risks?

It seems there is constant hand wringing about the risks around the Chinese economy with the common concerns being around unbalanced growth, debt, the property market, the exchange rate and capital flows and a “hard landing”. This angst is understandable to some degree. Rapid growth as China has seen brings questions about its sustainability. And China is now the world’s

Read MoreIt seems there is constant hand wringing about the risks around the Chinese economy with the common concerns being around unbalanced growth, debt, the property market, the exchange rate and capital flows and a “hard landing”. This angst is understandable to some degree. Rapid growth as China has seen brings questions about its sustainability. And China is now the world’s second largest economy, its biggest contributor to growth and Australia’s biggest export market so what happens in China has big ramifications globally. But despite all the worries it keeps on keeping on and recently growth has been relatively stable. This note looks at China’s growth outlook, the main risks and what it means for investors and Australia.

Stable growth, benign inflation

Chinese growth slowed through the first half of this decade culminating in a growth and currency scare in 2015 which saw Chinese policy swing from mild tightening towards stimulus. This has seen pretty stable growth since 2016 of around 6.8% year on year. Consistent with this, business conditions PMIs have also been stable (see the next chart) and uncertainty around the Renminbi has fallen & capital outflows have slowed.

Source: Bloomberg, AMP Capital

April data saw industrial production and profits accelerate but investment and retail sales slow a bit. Electricity consumption, railway freight and excavator sales have lost momentum from their highs. But the overall impression is that growth is still solid.

Source: Bloomberg, AMP Capital

While there is a need for China to rebalance its growth away from investing for exports, the slowdown in investment growth to below that for retail sales, imports growing faster than exports and the shrinkage in China’s current account deficit from 10% of GDP to 1% of GDP suggests this occurring.

Meanwhile, inflation in China is benign with producer price inflation around 3% and consumer price inflation around 2%.

Source: Domain, AMP Capital

Policy neutral

Chinese economic policy has been relatively stable recently. There has been some talk of boosting domestic demand and bank required reserve ratios have been cut. But the latter appears to have been to allow banks to repay medium term loan facilities, interest rates have been stable and growth in public spending has been steady at 7-8% year on year.

Growth and inflation outlook

We expect Chinese growth this year to slow a bit as investment slows further to around 6.5% and consumer inflation of 2-3%.

Key risks facing China

There are four key risks facing China. First, the policy focus could shift from maintaining solid growth to speeding up medium-term economic reforms and deleveraging (or cutting debt ratios) that could threaten short-term economic growth. Some expected this to occur after the 19th National Congress of the Communist Party was out of the way late last year. And the removal of term limits on President Xi Jinping could arguably make him less sensitive to a short-term economic downturn. However, so far there is no sign of this and the authorities seem focused on maintaining solid growth.

Second, China’s rapid debt growth could turn sour. Since the Global Financial Crisis, China’s ratio of non-financial debt to GDP has increased from around 150% to around 260%, which is a faster rise than has occurred in all other major countries.

Source: RBA, AMP Capital

This has been concentrated in corporate debt and to a lesser degree household debt and has been made easier by financial liberalisation and a lot of the growth has been outside the more regulated banking system in “shadow banking”. An obvious concern is that when debt growth is rapid it results in a lot of lending that should not have happened that eventually goes bad. However, China’s debt problems are different to most countries. First, as the world’s biggest creditor nation China has borrowed from itself – so there’s no foreigners to cause a foreign exchange crisis. Second, much of the rise in debt owes to corporate debt that’s partly connected to fiscal policy and so the odds of government bailout are high. Finally, the key driver of the rise in debt in China is that it saves around 46% of GDP and much of this is recycled through the banks where it’s called debt. So unlike other countries with debt problems China needs to save less and consume more and it needs to transform more of its saving into equity rather than debt. Chinese authorities have long been aware of the issue and growth in shadow banking and overall debt has slowed but slamming on the debt brakes without seeing stronger consumption makes no sense.

Third, the risk of a trade war has escalated with Trump threatening tariffs on $50-150bn of imports from China and restrictions on Chinese investment in the US and China threatening to reciprocate. While “constructive” negotiations have commenced and have seen China commit to buying more from the US & to strengthen laws protecting intellectual property which saw the US initially defer the tariffs and restrictions, Trump has indicated that they will be implemented this month which looks to be aimed at prodding China to move rapidly (and appeasing his base). Ultimately, we expect a negotiated solution, but the risks are high and a full-blown trade war with the US could knock 0.5% or so off Chinese short-term growth.

Finally, with the Chinese residential property market slowing again there is naturally the risk that this could turn into a slump. It’s worth keeping an eye on but absent an external shock looks doubtful. The “ghost cities” paranoia of a few years ago – it first aired on SBS TV way back in 2011 – has clearly not come to much. It’s doubtful China ever really had a generalised housing bubble: household debt is low by advanced country standards; house prices haven’t kept up with incomes; and while there’s been some excessive supply, this is not so in first tier cities; and the quality of the housing stock is low necessitating replacement. So, I think the property crash fears continue to be exaggerated and the latest bout of weakness in prices looks to be just another cyclical downswing in China of which there have been several over the last decade.

Our assessment remains that these risks are manageable, albeit the trade war risk is the hardest for China to manage given the erratic actions of President Trump. The Chinese Government has plenty of firepower to support growth though, so a “hard landing” for Chinese growth remains unlikely for now.

The Chinese share market

Since its low in January 2016 the Chinese share market has had a good recovery. But Chinese shares are trading on a price to earnings ratio of 12.8 times which is far from excessive.

With valuations okay and growth continuing, Chinese shares should provide reasonable returns, albeit they can be volatile.

Implications for Australia – not yet 2003, but still good

Solid growth in China should help keep commodity prices, Australia’s terms of trade and export volume growth reasonably solid. This, along with rising non-mining investment and strong public investment in infrastructure, will offset slowing housing investment and uncertainty over the outlook for consumer spending and will keep Australian economic growth going. However, with strong resources supply (and still falling mining investment) we are a long way from the boom time conditions of last decade and growth is likely to average around 2.5-3%. Rising US interest rates against flat Australian rates suggests more downside for the $A, but solid commodity prices should provide a floor for the $A in the high $US0.60s.

Key implications for investors

-

Chinese shares remain reasonably good value from a long- term perspective, but beware their short-term volatility.

-

Solid Chinese growth should support commodity prices and resources shares

Source: AMP Capital 04 June 2018

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.