Provision Newsletter

The RBA hikes rates by another 0.25% – are we there yet?

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

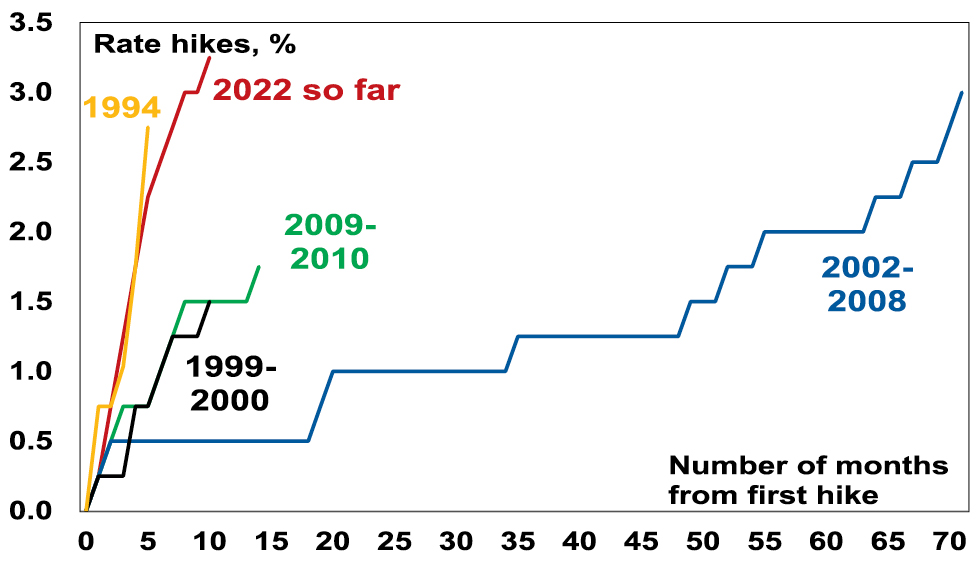

IntroductionThe RBA raised its cash rate by another 0.25% taking it to 3.35%. This is the ninth consecutive rate hike in a row over ten months totalling 325 basis points and exceeds the 2002-2008 tightening cycle (of 300 basis points over 71 months) making it the biggest tightening

Read MoreDr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

The RBA raised its cash rate by another 0.25% taking it to 3.35%. This is the ninth consecutive rate hike in a row over ten months totalling 325 basis points and exceeds the 2002-2008 tightening cycle (of 300 basis points over 71 months) making it the biggest tightening cycle since the 1980s. Prior to 1990 the RBA cash rate was not officially announced, and short-term rates were very volatile. In the period January 1988 to November 1989 the overnight cash rate rose from 10.6% to 18.2% but mortgage rates were more regulated then and “only” rose from 13.5% to 17%.

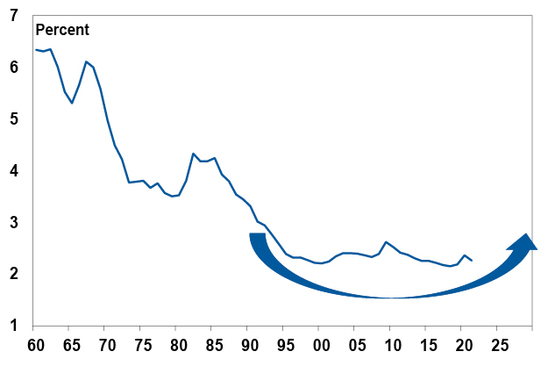

RBA rate hiking cycles since the 1990s

Source: RBA, AMP

In justifying another hike, the RBA noted that: inflation is at its highest since 1990 with underlying inflation higher than expected; the labour market remains tight; wages growth is expected to pick up; and its “priority is to return inflation to [the 2-3%] target”. The RBA also reiterated that: monetary policy operates with a lag; and it wants to keep the economy on an even keel. It made no significant changes to its forecasts and still sees growth slowing to 1.5% this year, unemployment rising to 3.75% and inflation slowing to 4.75%. But compared to its last post meeting Statement in December the RBA has become more hawkish most likely as a result of the stronger than expected rise in underlying inflation. In particular, the RBA noted that “the Board expects to increase interest rates further over the months ahead,” but removed the qualifier that “it is not on a pre-set course” (which had been interpreted as opening the door to a pause).

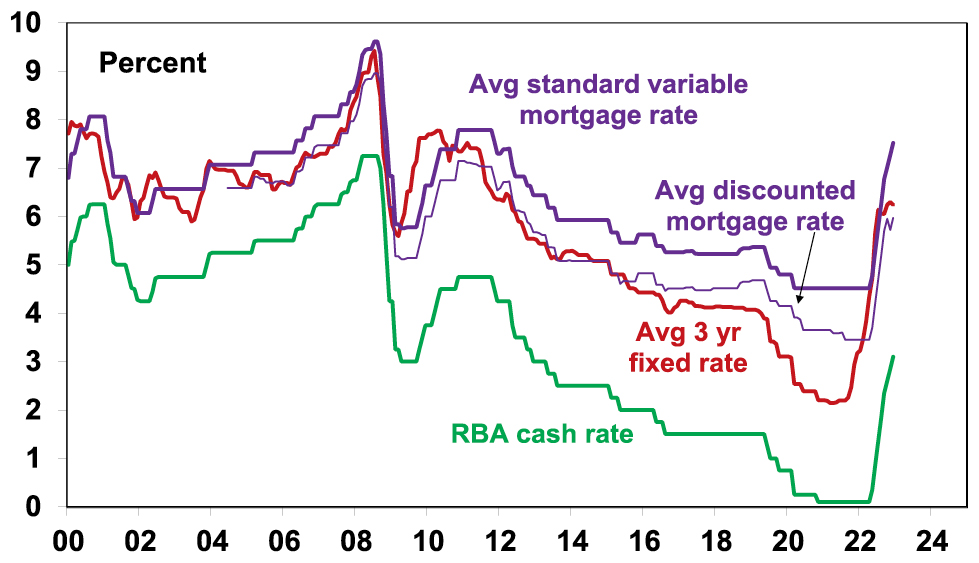

Banks are likely to pass the hike on in full taking variable mortgage rates to their highest in 11 years.

Australian interest rates still on the rise

Source: RBA, Bloomberg, AMP

Are we there yet?

While the RBA stepped up its hawkishness and another rate hike now looks likely next month, its commentary is not necessarily a great guide to what happens with rates – just a bit more than a year ago it didn’t expect rates to start rising until 2024 at the earliest! What happens to inflation and growth will be key. Given the experience of the last year one has to be humble in trying to predict the cash rate peak. Prior to the December quarter CPI release we thought the RBA would leave rates on hold at this month’s meeting! And some argue there are still many hikes ahead of us. So, it’s worth considering both sides of the argument.

The case for much higher interest rates

The case for still much higher interest rates rests on the following:

-

Inflation in Australia is still rising.

-

The labour market remains very tight – with the sum of unemployment and underemployment near their lowest since the early 1980s potentially driving much higher wages and a wage-price spiral.

-

Against this backdrop and given the 1970s experience the RBA needs to keep demonstrating its resolve to get inflation back down to keep inflation expectations down – otherwise it will get harder to tame.

-

Simple monetary policy rules suggest the cash rate should be much higher. For example, the most common rule called The Taylor Rule – formulated by US economist John B Taylor 30 years ago – posits that the official interest rate should equal the inflation rate plus the neutral real interest rate plus 0.5 times the gap between the current and target inflation rate and 0.5 times the output gap (ie, the gap between actual & potential GDP) or alternatively the gap between the unemployment rate and the non-accelerating inflation rate of unemployment (NAIRU). In fact, given the high starting point for the inflation rate (7.8%), a neutral rate of 1% and the big gap between inflation and the target inflation rate (2.5%) and unemployment being below NAIRU a standard specification of the Taylor Rule suggests the cash rate should maybe be around 11% – a level not seen since the early 1990s!

-

Other central banks all have higher rates, viz US Fed 4.5-4.75%; the BoE 4%; BoC 4.5%, RBNZ 4.25%. The ECB is lower at 3% but it started later.

-

The economy so far has been resilient with households supported by $250bn or so in extra saving built up in the pandemic lock down years.

Based on this it can be argued that interest rates need to rise a lot further – with several economists expecting the cash rate to rise above 4%.

The case for rates being near the top

The counterargument suggesting that we may be at or close to the top on rates is based on the following:

-

First, monetary policy operates with a lag. It takes 2-3 months for RBA rate hikes to impact actual variable rate mortgage payments and then several months before this impacts spending. There are then flow on effects to jobs and businesses with feedback impacts on households which can take a year. And this lag may have been lengthened by the rise in fixed rate mortgages around 2020-21 and the reopening boost to spending. The lag was clearly evident in the late 1980s but ignorance of it contributed to the severity of the early 1990s recession.

-

Second, inflationary pressure is easing globally. This is evident in global business surveys showing reduced delivery times and falling work backlogs, lower freight costs, lower metal and grain prices, and falling input and output prices. US money supply which surged ahead of the US inflation spike is falling. US inflation peaked mid-year at 9.1% and has fallen to 6.5% and inflation in Europe, the UK and Canada appears to have peaked. Australian inflation appears to be following the US by six months (due partly to a later reopening in the economy and later surge in energy prices), suggesting it peaked here last quarter.

-

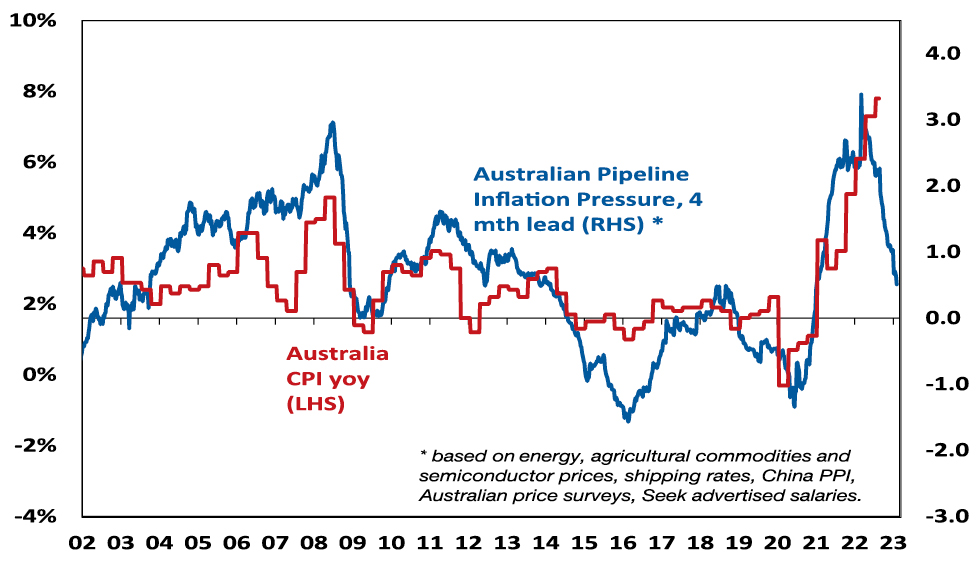

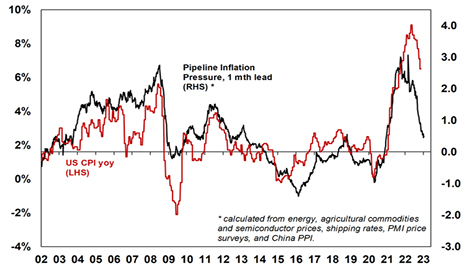

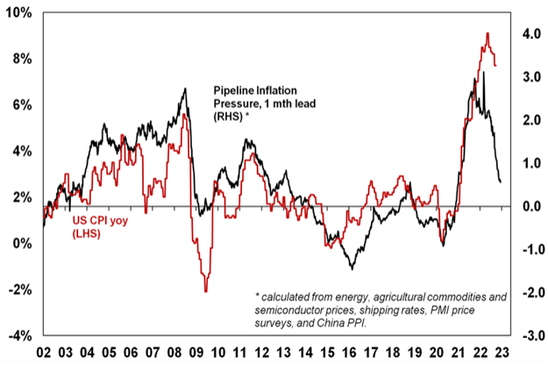

Third, there are signs Australian inflation is peaking with business surveys showing a downtrend in input and output price readings, low work backlogs & a falling capacity utilisation. Reflecting this and global indicators, our Australian Pipeline Inflation Indicator is falling sharply.

Australia Pipeline Inflation Indicator

Similar to our US Inflation Indicator but has more Aust components, Source: Bloomberg, AMP

-

Fourth, some of the components which drove inflation so high are unlikely to be repeated: the 10.9% December quarter rise in travel costs will start to fade as travel and travel industry capacity return to normal; dwelling purchase costs (up 18%yoy) are now slowing; petrol prices appear to be stabilising; and electricity prices this year may be lower than previously expected with falling gas and coal prices.

-

Fifth, while the Taylor Rule is a useful framework its prescription varies dramatically depending on the assumptions used, it makes no allowance for whether inflation psychology is entrenched or not (if it is like in the 1970s and 1980s then much higher rates are needed – but that looks unlikely) and it makes no allowance for the high level of household debt compared to the past and the degree of reliance of households on short dated mortgages compared to other countries (eg in the US 95% of mortgages are at fixed 30 year mortgage rates).

-

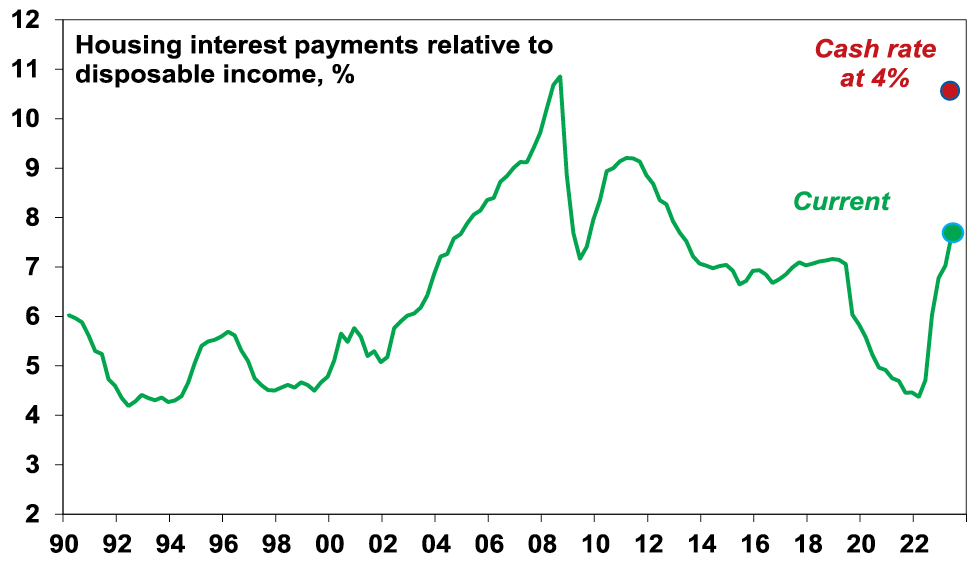

Specifically in relation to household debt, given the almost three-fold increase in the household debt to income ratios over the last 30 years, a 17% mortgage rate in 1989 – which preceded the early 1990s recession – is roughly equivalent to a 6% variable mortgage rate today and we are already pushing through that. A variable rate borrower on an existing $500,000 mortgage (which is the average) will see roughly another $80 added to their monthly payment from today’s RBA hike which will take the total increase in their monthly payments since April to nearly $1000 a month. That’s an extra $12,000 a year which is a massive hit to household spending power. And roughly two thirds of the 40% of mortgaged households with fixed rates (roughly about 1 million households) will see a 2 or 3 fold increase in their payments when their fixed term expires by the end of the year. And the RBA’s interest rate hikes have now exceeded the 2.5% mortgage rate serviceability buffer that applied up to October 2021 and the 3% since. The surge in interest rates has already pushed mortgage interest payments as a share of household income back to levels not seen since early last decade. A rise in the cash rate to 4% would push the interest payment share to near a record high and total mortgage repayments (ie, interest and principal) as a share of income to record highs. The hit to spending power for households with a mortgage (who tend to vary their spending more than older Australian’s with big bank deposits) is likely to drive a big slowing in consumer spending.

Household housing interest payments v disposable income

Source: ABS, RBA, AMP

-

Sixth, there is increasing evidence rate hikes are getting traction: housing related indicators are all very weak; the 9% fall in home prices will depress consumer spending via a negative wealth effect; consumer confidence remains depressed; retail sales are falling in real terms; and there are some signs of slowing jobs growth. Slower demand in the economy will further reduce inflationary pressures. This may become more evident as the reopening bounce (“revenge” spending) wears off.

-

Finally, Australia is not acting alone as global rate hikes are slowing growth in advanced countries which in turn will slow global inflation pressures – so other central banks are doing part of the RBA’s job.

Concluding comment

On balance, while the RBA now looks likely to hike rates again by another 0.25% next month – continuing much further down the path of rate hikes in response to inflation which is a lagging indicator while ignoring the lagged flow through of rate hikes to the economy, signs of slowing demand and improving supply risks plunging the economy into a recession we don’t have to have. So, despite being premature so far, we still see the RBA as being close to the peak with rates. Our base case is now for one more 0.25% hike next month, followed by a lengthy peak as it becomes clearer that inflationary pressures are easing and growth is slowing, ahead of the start of rate cuts late this year or early next year.

Source: AMP Capital February 2023

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Seven reasons why Australian shares are likely to outperform global shares over the medium term

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

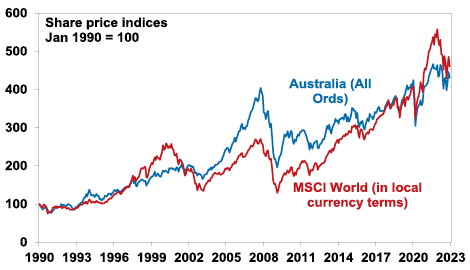

IntroductionSince the March 2009 Global Financial Crisis (GFC) low in share markets, Australian shares are up 138%, compared to a 310% gain in global shares in local currency terms and a 500% gain in US shares.

Australian and global shares

Source: Bloomberg, AMP

Last year though Australian shares outperformed global shares,

Read MoreDr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

Since the March 2009 Global Financial Crisis (GFC) low in share markets, Australian shares are up 138%, compared to a 310% gain in global shares in local currency terms and a 500% gain in US shares.

Australian and global shares

Source: Bloomberg, AMP

Last year though Australian shares outperformed global shares, helped by strong commodities and a less hawkish RBA. The big question is whether the structural underperformance by Australian shares since 2009 is over?

Why have Australian shares underperformed?

To get a handle on the future, it’s useful to understand the past. The underperformance of Australian shares since 2009 reflects a mix of:

-

Payback for its huge outperformance in the 2000s – Australian shares go through periods of relative out & underperformance. This can be seen in the next chart that shows the relative decade by decade real returns of global and Australian shares since 1940. Australian shares outperformed in the 1940s, unperformed in the 1950s, outperformed in the 1960s resources boom years, underperformed in the high inflation 1970s and 80s, outperformed in the 1990s (although this was marginal and Australia underperformed in the second half of the 1990s when the tech boom raged), outperformed dramatically in the resources boom of the 2000s and underperformed in the 2010s.

Australian versus global shares returns – mean reversion

Source: ABN-Amro Global Investment Returns Yearbook, Bloomberg, AMP

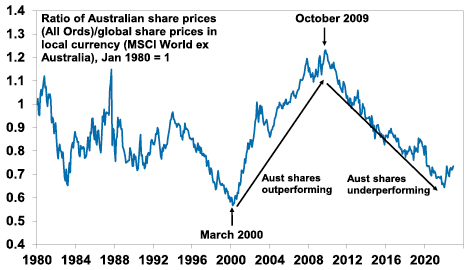

The swings in relative performance can also be seen in the next chart which shows the ratio of Australian share prices to global share prices.

Australian shares prices relative to global share prices

Source: Bloomberg, AMP

-

After underperforming global shares in the tech boom in the second half of the 1990s, Australian shares came roaring back in the 2000’s resources boom. This meant the 2007 high for Australian shares was a much higher high than for global shares which spun their wheels in the 2000s. So, the poor relative performance of Australian shares since 2009 is partly payback for their outperformance in the 2000s.

-

The slump in commodity prices from 2011 – this weighed heavily on Australian resources shares through much of last decade.

-

Relatively tighter monetary policy in Australia for much of the post GFC period – whereas the US, Europe and Japan had near zero interest rates and quantitative easing, Australia has had much higher rates and no money printing until the pandemic. In fact, the relative underperformance started in October 2009 when the RBA raised rates post GFC which wasn’t followed by other major countries.

-

The surge in the $A to $US1.10 in 2011 – this reduced the competitiveness of Australian companies which takes time to reverse.

-

Property crash phobia – foreign investor fear of a crash in Australia’s expensive housing market has been a periodic theme over the last decade leading many foreign investors to be cautious of Australia.

-

Worries about the deteriorating relationship with China – this started in 2018 with President Trump’s trade war but was accentuated through the pandemic. It arguably resulted in foreign investors demanding a risk premium to invest in the $A and Australian shares.

-

A low exposure to pandemic winners – like tech stocks, which helped the US share market and hence global shares in 2020 & 2021.

Are high dividend payouts to blame?

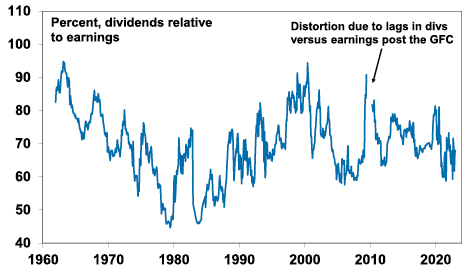

An often expressed view is that Australian companies are not investing because shareholders want high dividends and this could be causing poor profit growth & share returns. This is unlikely. The dividend payout ratio (ie dividends relative to earnings) is not out of line with its historic norm.

Australian dividend payout ratio

Source: Bloomberg, RBA, AMP

Australia’s high dividend payouts are in fact healthy from a long-term perspective. There is evidence that high payouts actually drive higher earnings growth and share returns as: high dividend payouts mean less risk of poor investment decisions from retained earnings; they are indicative of corporate confidence about future earnings; & they indicate earnings are real and not an accounting fiction.

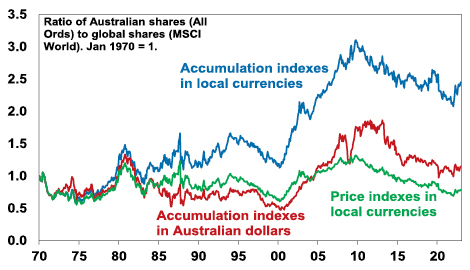

In fact, because Australian shares pay relatively high dividend yields (around 4.4%) compared to global shares (2.5%) they should be included in comparisons of Australian with global share market returns. The next chart compares the relative performance of Australian to global shares since 1970 in terms of: relative share prices in local currency terms (green line); relative total returns ie with dividends added in (blue line); and relative total returns with global shares in Australian dollars (red line).

Australian shares relative to global shares allowing for dividends and currency movements

Source: Thomson Reuters, Bloomberg, AMP

A rising ratio means Australian outperformance and vice versa. Several things stand out. First over long periods of time and when dividends are allowed for Australian shares have had better returns than global shares. Since 1970 Australian shares have returned (capital growth plus dividends) 10.1% per annum compared to 8.2% pa for global shares in local currency terms. The falling $A over this period has enhanced the return from global shares to 9.8% pa but they still underperformed Australian shares. Second, the swings in the relative performance of Australian shares are apparent if dividends and currency movements are allowed for or not – in particular in the big outperformance in the 2000s and underperformance since 2009. Since October 2009, when Australian shares peaked relative to global shares, Australian shares have returned 7.7% pa compared to 9.7% pa from global shares in local currencies or 11.3% pa in $A terms (as the $A fell).

Seven reasons Australia’s underperformance is likely over

Over the last year Australian shares have outperformed global shares and the various comparisons in the last chart have hooked higher. It could just be noise, but several fundamental considerations suggest that the structural relative underperformance since 2009 is likely to be over:

-

Mean reversion – after 12 years of underperformance & the reversal of the 2000s outperformance Australian shares are due for a lengthy period of outperformance. Consistent with this, Australian shares are trading on a lower forward price to earnings multiple of 14.5 times than global shares on 15.3 times & US shares on 17.1 times.

-

A new super cycle in commodities – the commodity price slump from their 2008-2011 highs looks to be over with commodities embarking on a new super cycle bull market driven by constrained supply after low levels of investment and low inventories for most commodities, decarbonisation driving increased demand for metals and increased defence spending on the back of increased geopolitical tensions which is metal intensive. This will benefit Australia’s resource stocks.

-

The $A is no longer expensive – the surge in the $A to $US1.10 of 2011 has long ago reversed with the $A hitting a low of $US0.57 in 2020 & $US0.62 last year making Australian companies more competitive.

-

Stronger growth potential – Australia’s potential growth rate remains higher than the US, Europe & Japan due to higher population growth.

-

Relatively high dividends – Australian shares pay a higher dividend yield than traditional global shares: 4.4% versus 2.5%. This is important because dividend payments are a big chunk of the return an investor will get and so the higher the better. Franking credits add around 1.3%pa to the post tax return for Australia-based investors.

-

Less aggressive monetary tightening – RBA monetary policy is no longer relatively tight compared to other major central banks, notably the Fed. It has been taking a more balanced approach to returning inflation to target. Higher than expected December quarter inflation is a concern and is now likely to see the RBA hike rates by another 0.25% in February. But its likely to be the peak in inflation as supply is improving, freight costs have fallen and demand is slowing and its unlikely to see the RBA adopt a more aggressive policy compared to other major countries.

-

A thawing in the China relationship – the risk of a sharp deterioration in the trade relationship with China appears to be receding (at least for a while) helped by a change of Government in Australia.

Finally, while Australian property prices likely have more downside there is no sign of a property crash dragging down banks and the economy into recession. In the absence of much higher interest rates this looks unlikely.

Concluding comment

The period of underperformance in Australian shares compared to global shares since 2009 is likely to be over. Expect a 5-10 year period of trend outperformance, albeit there will be bumps along the way.

Source: AMP Capital January 2023

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

2023 – a list of lists regarding the macro investment outlook

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

IntroductionAfter very strong returns in 2021 thanks to reopening from Covid restrictions and stimulatory fiscal and monetary policies, 2022 was a rough year reflecting high inflation, a surge in interest rates and bond yields, geopolitical issues (notably the invasions of Ukraine) and recession worries. This saw average balanced

Read MoreDr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

After very strong returns in 2021 thanks to reopening from Covid restrictions and stimulatory fiscal and monetary policies, 2022 was a rough year reflecting high inflation, a surge in interest rates and bond yields, geopolitical issues (notably the invasions of Ukraine) and recession worries. This saw average balanced growth super funds lose around 5% (or around 12% after inflation), as both shares and bonds lost value, after returning 14% in 2021. Over the last five years, they have returned around 5.5% pa with a pattern of successive strong followed by weak years, etc, since 2017.

Balanced growth superannuation fund returns

Source: Mercer Investment Consulting, Morningstar, AMP

Will the poor returns continue, or can we expect a rebound? Here is a simple point form summary of key insights and views on the outlook.

Five lessons for investors from 2022

-

Inflation was not dead (just resting) – the pandemic driven surge in money supply and reopening driven surge in demand against a backdrop of supply constraints released it from its long slumber.

-

To control inflation, central banks have to act and sound very tough. They started a bit late initially, but got there eventually in 2022.

-

Share markets go through periodic rough patches – and high inflation and rapidly rising interest rates are not good for them.

-

Geopolitics matters – particularly if war disrupts commodity supply.

-

Turn down the noise – investors are now bombarded with irrelevant, low quality and conflicting information which confuses and adds to uncertainty. This was particularly evident in 2022. The best approach is to turn down the noise and stick to a long-term investment strategy.

Nine reasons for optimism

2022 was not so good and economic growth will slow sharply this year thanks to rate hikes and cost of living pressures (with a high risk of recession in the US and Europe), but there are several reasons for optimism.

-

Long term inflation expectations remain low – while they were a bit slow initially central banks swung into inflation fighting action with rapid rate hikes and tough rhetoric showing they learned the key lesson of the 1970s – which is to keep inflation expectations down.

-

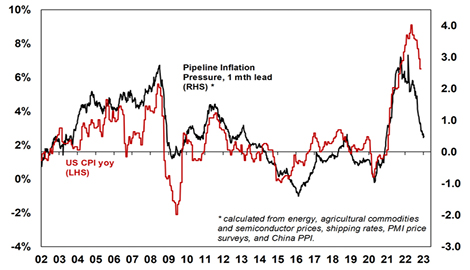

Inflation has likely peaked – this is most evident in the US where inflation led on the way up & is likely now leading on the way down. US inflation peaked mid last year & our Pipeline Inflation Indicator points to a sharp fall ahead. Labour market tightness is showing signs of easing which should take pressure of wages – this is flowing from slowing demand and in Australia will be helped foreign workers returning.

AMP Pipeline Inflation Indicator

Source: Bloomberg, AMP

-

Key central banks have likely seen or are close to peak hawkishness – this flows from the likely fall in inflation and signs of cooling demand.

-

China’s move away from zero Covid will provide an offset to weaker US and European growth – albeit after an initial set back as new cases surged, much like they did in other countries that reopened.

-

The US dollar looks to have peaked – which should ease debt servicing pressure in emerging countries with US dollar denominated debt.

-

Vaccines, anti-virals and with less harmful mutations have allowed the world to start moving on from Covid. China is now playing catch up.

-

In Australia, the less aggressive RBA along with other factors (see below), should help us avoid recession.

-

Geopolitics may not be as threatening. Western democracies united and authoritarianism/strongmen leaders took a hit in 2022 – with Putin weakened by the mess in Ukraine, China’s difficulties exiting zero-Covid and Trump on the nose after the US mid-terms. The war in Ukraine may not get any more threatening, there are signs of a thaw in China relations & there are no major elections in key countries in 2023.

-

While US mid-term election years are often poor for shares (as seen in 2022), the 12 months after the US mid-terms is normally strong.

Five reasons Australia is likely to avoid a recession

A slump in consumer spending (thanks to rate hikes, cost of living pressures and falling property prices) along with weaker global growth will see Australian growth slow to around 1.5% this year. The risk of recession is high, but it’s likely to be avoided.

-

The RBA is less aggressive and less likely to overtighten compared to other major central banks.

-

Thanks to poor weather, material and labour shortages, there is a large pipeline of home building approved but yet to be completed.

-

The business investment outlook remains solid.

-

A rebound in Chinese growth is likely to support export volumes and prices. After a rough start to the year due to the surge in Covid cases with reopening, Chinese growth is expected to rebound to around 6% this year thanks to reopening providing an offset to weakness in other countries. The return of Chinese students, tourists and relaxation of export bans (notably on coal) could add around 1% to Australian growth spread over a couple of years.

-

Immigration is rebounding rapidly, which means more workers and support for economic growth.

These considerations should also support a continuation of the relative outperformance of Australian shares compared to global shares.

Key views on markets for 2023

Easing inflation pressures, central banks moving to get off the brakes, the anticipation of stronger growth in 2024 and improved valuations should make for better returns in 2023. But there are likely to be bumps on the way – particularly regarding recession risks – & this could involve a retest of 2022 lows or new lows in shares before the upswing resumes.

-

Global shares are expected to return around 7%. The post mid-term election year normally results in above average gains in US shares, but US shares are likely to remain a relative underperformer compared to non-US shares reflecting higher PE multiples. The $US is likely to weaken further which should benefit emerging and Asian shares.

-

Australian shares are likely to outperform global shares again, helped by stronger economic growth than in other developed countries and ultimately stronger growth in China supporting commodity prices helped by the grossed-up dividend yield of around 5.5%.

-

Bonds are likely to provide returns around running yield or a bit more, as inflation slows and central banks become less hawkish.

-

Unlisted commercial property and infrastructure are expected to see slower returns, reflecting the lagged impact of weaker share markets and higher bond yields on valuations.

-

Australian home prices are likely to fall another 9% or so as rate hikes continue to impact, resulting in a top to bottom fall of 15-20%, but with prices expected to bottom around September, ahead of gains late in the year as the RBA moves toward rate cuts.

-

Cash and bank deposits are expected to provide returns of around 3%, reflecting the back up in interest rates through 2022.

-

A rising trend in the $A is likely this year, reflecting a downtrend in the overvalued $US, the Fed moving to cut rates and solid commodity prices helped by stronger Chinese growth.

Five reasons to expect continuing volatility

While investment returns should improve, volatility is likely to stay high.

-

Growth is slowing in key advanced countries – with uncertainty about the depth of any downturn and the flow on to profits.

-

Inflation – while its likely to slow further it will still be high for a while.

-

Quantitative tightening (withdrawing the cash pumped into economies through the pandemic) will accentuate monetary tightening to an uncertain degree.

-

Geopolitical risk around Ukraine, China and Iran is still high.

-

Raising the US debt ceiling as needed around mid-year could be fraught given the increased power of fiscal conservatives in the House of Representatives.

Five things to watch

-

Inflation – if it continues to rise, central banks will be more hawkish than we are allowing for, risking deep recession.

-

Recession – a mild recession in US and Europe should be manageable but a deep recession will mean significantly more downside in shares.

-

US politics – the return to divided government, with GOP controlling the House, means a high risk of brinkmanship around raising the debt ceiling, causing volatility in markets as we saw in 2011 and 2013.

-

Geopolitics – with the war in Ukraine, China tensions around Taiwan and the risk of increased tensions around Iran are the main risks.

-

Australian home prices – a sharper than expected fall as fixed rates reset and unemployment rises, could cause financial stability issues.

Nine things investors should remember

-

Make the most of compound interest to grow wealth. Saving regularly in growth assets can grow wealth significantly over long periods. Using the “rule of 72”, it will take 144 yrs to double an asset’s value if it returns 0.5%pa (ie, 72/0.5) but only 14 yrs if the asset returns 5%pa.

-

Don’t get thrown off by the cycle. Falls in asset markets can throw investors of a well-considered strategy, destroying potential wealth.

-

Invest for the long-term. Given the difficulty in timing market moves, for most it’s best to get a long-term plan that suits your wealth, age & risk tolerance & stick to it.

-

Diversify. Don’t put all your eggs in one basket.

-

Turn down the noise. This is critical with the information overload coming from social media, and mainstream media going down the clickbait path.

-

Buy low, sell high. The cheaper you buy an asset, the higher its prospective return will likely be and vice versa.

-

Avoid the crowd at extremes. Don’t get sucked into euphoria or doom and gloom around an asset.

-

Focus on investments you understand offering sustainable cash flow. If it looks dodgy, hard to understand or has to be justified by odd valuations or lots of debt, then stay away. There is no free lunch!

-

Seek advice. Investing can get complicated and its often hard to stick to a long-term investment strategy on your own.

Source: AMP Capital January 2023

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Review of 2022, outlook for 2023

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

2022 – from Covid to inflation & surging interest ratesThe good news is that 2022 finally saw the world shake off the grip of Coronavirus as it transitioned from a pandemic to endemic (albeit it’s still causing problems in China). However,

Read MoreExpect a rough ride, but better returns

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

2022 – from Covid to inflation & surging interest rates

The good news is that 2022 finally saw the world shake off the grip of Coronavirus as it transitioned from a pandemic to endemic (albeit it’s still causing problems in China). However, the past year turned out far more difficult for investors than might have been thought a year ago:

-

Inflation, which already rose in 2021 surged to levels not seen for decades, largely reflecting pandemic related distortions to supply and reopening & a stimulus driven surge in demand & floods in Australia.

-

Russia invaded Ukraine, leading to a surge in energy & food prices.

-

Central banks moved to aggressively withdraw monetary stimulus and raised interest rates at the fastest pace seen in decades to deal with inflation and rising inflation expectations.

-

Bond yields surged in response to the rise in inflation & interest rates.

-

Chinese growth fell sharply, reflecting its zero-Covid policy and a continuing property downturn despite policy stimulus.

-

Geopolitical tensions surged with war in Ukraine and worries about a Chinese invasion of Taiwan following President Xi Jinping’s power consolidation, although there were hopes of a thaw near year end.

-

As a result of all this, investors increasingly fretted about recession.

-

Tech stocks and crypto currencies, having been the biggest winners of the Covid lockdowns & easy money, were hit hard by reopening and monetary tightening, ultimately proving no hedge against inflation.

Growth was still ok – but a lot weaker than expected

Despite these problems, global GDP is still expected to have come in at around 3.2% which is weaker than the 5% or so growth expected a year ago and down from 6% in 2021, but still reasonable as reopening and stimulus helped. And in Australia, GDP is expected to have been around 3.5%, lower than expected a year ago and down from 4.8% in 2021, but still reasonable. The growth slowdown saw a slowdown in profits. But the main problem for investment markets was the rise in inflation, interest rates and bond yields.

Investment returns for major asset classes

|

Total return %, pre fees and tax |

2021 actual |

2022* actual |

2023 forecast |

|

Global shares (in Aust dollars) |

29.6 |

-7.4 |

4.0 |

|

Global shares (in local currency) |

24.3 |

-11.9 |

7.0 |

|

Asian shares (in local currency) |

-6.8 |

-18.0 |

10.0 |

|

Emerging mkt shares (local currency) |

-0.2 |

-13.8 |

10.0 |

|

Australian shares |

17.2 |

2.2 |

10.0 |

|

Global bonds (hedged into $A) |

-1.5 |

-11.1 |

3.0 |

|

Australian bonds |

-2.9 |

-7.8 |

4.0 |

|

Global real estate investment trusts |

30.9 |

-23.0 |

9.0 |

|

Aust real estate investment trusts |

26.1 |

-17.1 |

9.0 |

|

Unlisted non-res property, estimate |

12.3 |

11.5 |

4.0 |

|

Unlisted infrastructure, estimate |

12.0 |

10.0 |

5.0 |

|

Aust residential property, estimate |

23.0 |

-7.0 |

-7.0 |

|

Cash |

0.0 |

1.0 |

3.1 |

|

Avg balanced super fund, ex fees & tax |

14.3 |

-3.0 |

6.3 |

* Year to date to Nov. Source: Thomson Reuters, Morningstar, REIA, AMP

-

Global shares had a rough year with a plunge of 23% into October on inflation, interest rate and recession worries, before a rally cut losses.

-

Chinese shares led the weakness, not helped by its zero Covid policy, followed by Asian shares, given their exposure to China and cyclical sensitivity. US shares also underperformed reflecting its high-tech exposure & aggressive Fed tightening.

-

Australian shares outperformed, helped by strong commodity prices and a relatively less hawkish RBA.

-

Government bonds slumped as yields surged on high inflation & rate hikes. Australian bonds had their worst year since 1973 or the 1930s.

-

Real estate investment trusts fell with the surge in bond yields.

-

Unlisted property & infrastructure returns remained strong, being less sensitive to short-term share market and bond yield moves.

-

Home prices fell sharply reflecting poor affordability after a boom &, particularly, as mortgage rates rose, reducing home buyer capacity.

-

Cash and bank term deposit returns improved but were still low.

-

The $A fell with share markets on growth concerns and relatively aggressive Fed rate hikes into October, before a partial recovery.

-

Balanced super funds had negative returns reflecting poor share and bond returns. This followed very strong returns in 2021.

2023 – lower inflation and lower growth

First the bad news: inflation is still way too high at around 7 to 11% in many advanced countries; tight labour markets risk wage-price spirals; central banks are still warning of more rate hikes; the risk of recession is high with inverted yield curves and weak confidence largely in response to rate hikes; the US has returned to divided Government with the risk of debt ceiling and funding standoffs; war continues in Ukraine; and tensions remain with China and Iran. Even Covid continues to disrupt – but mainly in China as cases surge as it reopens. These all suggest another volatile year and possibly continuation of the bear market in global shares.

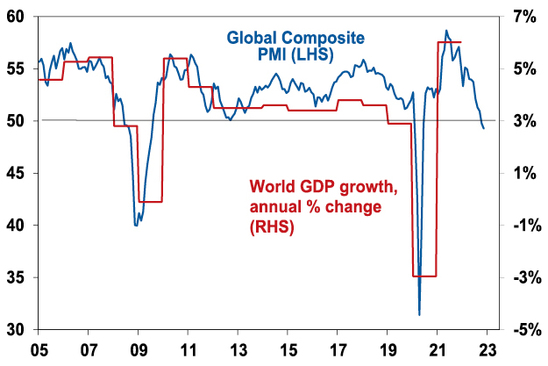

Global Composite PMI vs World GDP

PMIs are surveys of business confidence and conditions. Source: Bloomberg, IMF, AMP

However, there is reason for optimism. First, inflationary pressures may have peaked and are slowing rapidly (as reflected in our Pipeline Inflation Indicator): supply chain pressures have eased; demand is cooling; and labour markets are showing signs of topping out. In fact, it may only require a slight pull back in demand (to push capacity utilisation back down to normal & unemployment above the NAIRU – or non-accelerating inflation rate of unemployment, with the return of immigration helping in Australia) to further depress inflationary pressure significantly. This suggests inflation could fall faster than central banks expect in 2023.

AMP Pipeline Inflation Indicator

Note that this is more a guide to direction than level. Source: Bloomberg, AMP

Second, central banks are likely nearing the peak in rates. The Fed is already moving to slow hikes, but conditions are likely to be soft enough to allow it to pause from around March ahead of rate cuts later in 2023. Sure, its signalling more but just as its signals were too dovish a year ago its signals now are likely too hawkish! In Australia, we see the RBA as being at or close to the top (3.1% is our base case for the peak with 3.35% our risk case) as by February/March conditions are likely to be weak enough to allow a pause, ahead of rate cuts in late 2023/early 2024.

Third, it seems everyone is talking about recession for 2023, such that it’s a consensus call. The risk is very high (probably over 50% in the US and Europe) and this will likely keep markets volatile given the threat to earnings. But it may not turn out to be as bad as feared.

-

In the US it may just be a sharp slowdown or mild recession in 2023 – if the Fed starts to ease up on the brake soon and given the absence of other excesses that need to be unwound, eg, there has been no overinvestment in housing & capex and leverage is low.

-

Europe has moved away from Russian gas very quickly and providing its winter is mild, may continue to hold up better than feared.

-

Or lags in the way rate hikes impact may mean recession does not hit till 2024, meaning its too early for share markets to discount just yet.

-

After initial Covid related setbacks, Chinese growth is likely to rebound in 2023 as it reopens. Just like occurred in other countries upon reopening (recall Australia’s Omicron disruptions earlier in 2022) China is likely to see a surge in cases initially. But markets are likely to largely look through this to the reopening boost ahead which will provide an offset to slower growth in the US and Europe.

-

Australian growth is likely to slow but avoid recession, reflecting the less aggressive RBA, the pipeline of home building work yet to be completed and the strong business investment outlook.

Finally, geopolitics may not be so bad in 2023: there are no major elections in key countries in 2023; the war in Ukraine may not get any more threatening; and the Cold War with China may see a bit of a thaw.

Overall, global growth in 2023 is likely to be around 2.5%, well down from 6% in 2021, but not recession in aggregate. In Australia, growth is expected to slow to 1.5% in the year ahead. And inflation is likely to fall.

Implications for investors

Easing inflation pressures, central banks moving to get off the brakes, economic growth proving stronger than feared and improved valuations should make for better returns in 2023. But there are likely to be bumps on the way – particularly regarding recession risks – & this could involve a retest of 2022 lows or new lows in shares before the upswing resumes.

-

Global shares are expected to return around 7%. The post mid-term election year normally results in above average gains in US shares, but US shares are likely to remain a relative underperformer compared to non-US shares reflecting still higher price to earnings multiples (17.5 times forward earnings in the US versus 12 times forward earnings for non-US shares). The $US is also likely to weaken which should benefit emerging and Asian shares.

-

Australian shares are likely to outperform again, helped by stronger economic growth than in other developed countries and ultimately stronger growth in China supporting commodity prices and as investors continue to like the grossed-up dividend yield of around 5.5%. Expect the ASX 200 to end 2023 at around 7,600.

-

Bonds are likely to provide returns around running yield or a bit more, as inflation slows and central banks become less hawkish.

-

Unlisted commercial property and infrastructure are expected to see slower returns, reflecting the lagged impact of weaker share markets and higher bond yields (on valuations).

-

Australian home prices are likely to fall further as rate hikes continue to impact, resulting in a top to bottom fall of 15-20%, but with prices expected to bottom around the September quarter, ahead of gains late in the year as the RBA moves toward rate cuts.

-

Cash and bank deposits are expected to provide returns of around 3%, reflecting the back up in interest rates through 2022.

-

A rising trend in the $A is likely over the next 12 months, reflecting a downtrend in the now overvalued $US, the Fed moving to cut rates and solid commodity prices helped by stronger Chinese growth.

What to watch?

The main things to keep an eye on in 2023 are as follows:

-

Inflation – if it continues to rise, central banks will tighten more than we are allowing for risking deep recession.

-

US politics – the return to divided government, with GOP controlling the House, runs the high risk of a return to brinkmanship around the debt ceiling, causing volatility in markets as we saw in 2011 and 2013.

-

China issues – increased tensions around Taiwan are the main risk.

-

An escalation of the Ukraine conflict could adversely impact Europe.

-

Australian home prices – a sharper than expected fall as fixed rates reset and unemployment rises, could cause financial stability issues.

Source: AMP Capital December 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

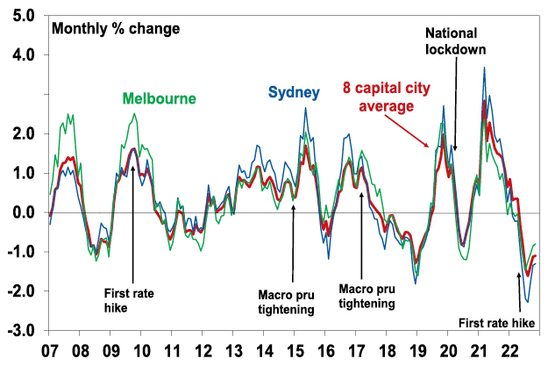

The home price slump continued in November, with still more to go

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

The slump in home prices continuesAfter surging by 28.6% from their pandemic lows early this year to record highs on the back of record low interest rates, home prices are continuing to plunge on the back of the fastest surge in interest rates since the early 1990s.

Read MoreDr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

The slump in home prices continues

After surging by 28.6% from their pandemic lows early this year to record highs on the back of record low interest rates, home prices are continuing to plunge on the back of the fastest surge in interest rates since the early 1990s. Australian capital city average dwelling prices fell another 1.1% in November according to CoreLogic, making it their seventh monthly decline in a row. Including regional dwellings, which fell another 0.9%, national dwelling prices fell 1%. Perth and Darwin remain relatively resilient as they are still getting over their post mining boom slumps. House prices are continuing to fall faster than unit prices, reflecting the much stronger boom in house prices and as unit prices are relatively supported by better affordability and tight rental markets.

Australian dwelling price growth, to November

|

|

Nov % chg |

Annual % chg |

% chg v high |

|

Sydney |

-1.3 |

-10.6 |

-11.4 |

|

Melbourne |

-0.8 |

-7.0 |

-7.1 |

|

Brisbane |

-2.0 |

3.3 |

-8.1 |

|

Adelaide |

-0.3 |

13.4 |

-0.9 |

|

Perth |

0.0 |

3.9 |

-0.7 |

|

Hobart |

-2.0 |

-4.1 |

-7.6 |

|

Darwin |

0.2 |

5.5 |

-0.7 |

|

Canberra |

-1.2 |

-1.3 |

-6.5 |

|

Capital city avg |

-1.1 |

-5.2 |

-7.5 |

|

Regional avg |

-0.9 |

3.3 |

-5.7 |

|

National avg |

-1.0 |

-3.2 |

-6.9 |

Source: CoreLogic, AMP

The key drivers of the downturn remain: poor affordability; rising mortgage rates; a rotation in spending from goods, including houses back to services; cost of living pressures, making it even harder to save for a deposit; and poor homebuyer confidence. Rising mortgage rates are the biggest driver of the slump as the surge in fixed mortgage rates, that started last year, and then variable rates has substantially reduced the amount new home buyers can borrow and hence pay for a home.

While the pace of monthly price declines has slowed in some cities, including the national average, this likely reflects the market getting used to the initial shock of rate hikes, bargain hunters taking advantage of lower prices and vendors holding off selling. Auction clearance rates also remain up from a low of around 50%, albeit in recent months they have stalled around 60% and volumes remain low.

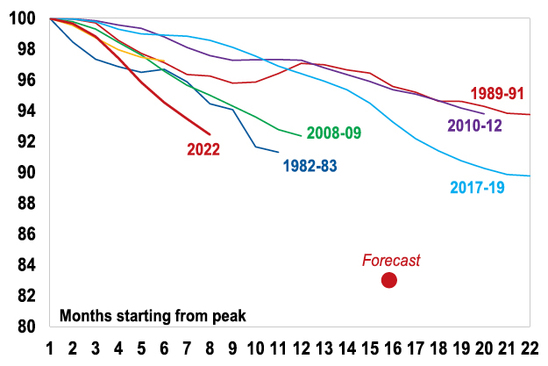

But with the full impact of rate hikes yet to be felt, interest rates still rising and the economy set to weaken, the slowdown in price falls in some cities is unlikely to presage an imminent bottoming in home prices. Past periods of property price falls experienced a few gyrations in the pace of price declines before prices ultimately bottomed, eg in the 2017-19 down cycle. See the next chart.

Average capital city home prices

Source: CoreLogic, AMP

So far national average property prices are down 6.9% from their high and average capital city home prices are down 7.5% both over seven months. This is the fastest pace of decline on CoreLogic records going back to 1980. The rapidity of the decline likely reflects the de facto tightening that started with rising fixed mortgage rates a year ago, the speed of RBA cash rate hikes (the fastest since 1994) and heightened sensitivity to rising rates due to high debt levels, along with the extent of the prior boom.

Australian Capital City Home Price Downturns (peak in prices indexed to 100)

Source: CoreLogic, AMP

Of course, average home price levels have still only seen a flick off the top after a huge boom. See the next chart.

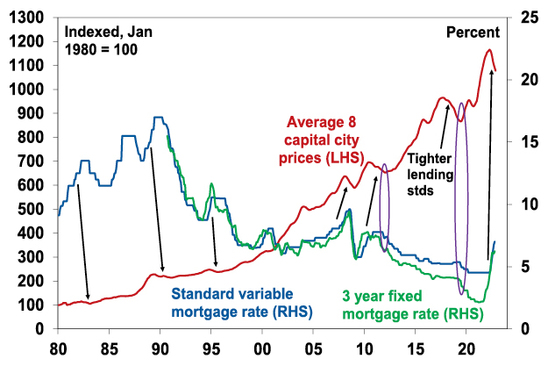

Australian property prices and interest rates

Source: CoreLogic, AMP

Outlook – we continue to expect average property prices to have a top to bottom fall of 15 to 20%

We expect average property prices to fall further into second half 2023 as rate hikes continue to flow through and economic conditions deteriorate:

-

the full impact of variable rate hikes has yet to be fully felt as it takes 2-3 months for RBA hikes to show up in actual mortgage payments;

-

we are expecting another 0.25% hike this month with the risk of another 0.25% in February and the money market is still expecting the cash rate to be raised to near 4% (from 2.85% currently);

-

two thirds of the 40% of households with a mortgage on fixed rates will see their mortgage rate reset from around 2% to around 5 or 6% by the end of next year. This is likely to result in a sharp rise in mortgage stress – this is the so called “fixed mortgage rate cliff”;

-

economic conditions are set to deteriorate next year as weaker global growth and rate hikes slow the economy & push up unemployment.

The combination will result in a further weakening in demand and a potential increase in supply as some financially stressed homeowners sell. In terms of the former, the next chart shows actual home prices compared to an estimate of what a buyer – with a 20% deposit, average full time earnings and mortgage payments assessed at 28% of their income – can afford to pay for a home. The shift in mortgage rates from 17% in 1989 to record lows in 2020 around 2-3% was the main enabler of the surge in home prices and price to income ratios. In other words, record low mortgage rates were reflected in record high home prices. While it can be seen from the chart that there are deviations and there are lots of other factors impacting home prices (supply, immigration, household size, taxation, help from “mum and dad”, home size and quality, and government incentives), over time home prices are tied to what people can afford to pay. But since April the amount an average new buyer can afford to pay has dropped by roughly 25% from around $600,000 to around $450,000. This demand side impact has been the key driver of home price falls so far, but suggests there is much more to go.

Australian Average Home Prices

Partly based on a Deutsche Bank analysis. Source: RBA, CoreLogic, AMP

Out of interest, while home prices have fallen 7% or so from their recent high, the time taken to save for a 20% deposit remains almost double what it was in the mid 1990s. The combination of the surge in interest rates and still sky high home prices relative to incomes, which necessitate very high debt levels, means affordability is almost as bad as its ever been.

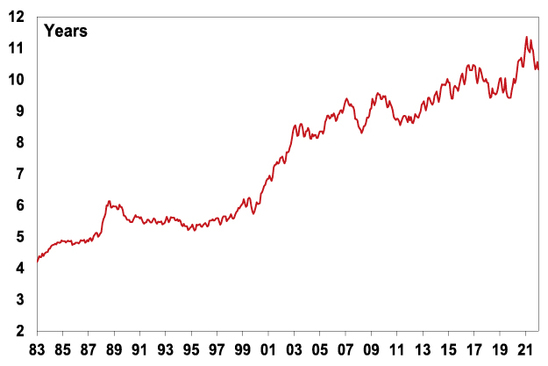

Years it takes to save for a 20% deposit

This assumes that the buyer saves 15% of their income each year. Source: RBA, CoreLogic, AMP

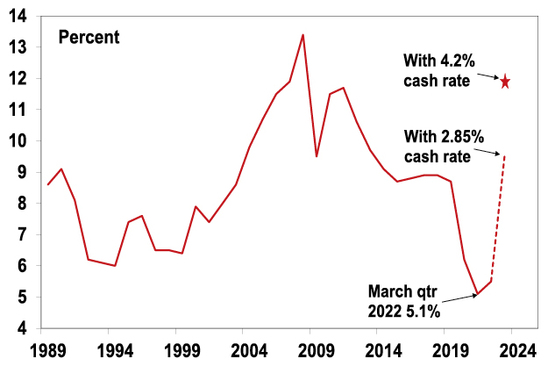

In terms of financial stress, with the 2.85% cash rate household interest payments as a share of income are already estimated to be at a near nine year high. Given record debt levels, further increases in mortgage rates will start to push total mortgage payments (principal and interest) to record highs relative to household income. This is likely to result in a sharp rise in mortgage stress – particularly as fixed rate loans reset next year.

Aust household interest relative to disposable income

Source: ABS, RBA, AMP

As a result of these demand and supply side considerations flowing from higher interest rates, we continue to expect national home prices will have a top to bottom fall of 15 to 20% out to around September quarter next year, of which we are only about 40% of the way through.

The main risks on the downside are that the RBA raises the cash rate to around 4% (as the money market is assuming) and the economy enters recession. The RBA has already raised rates by more than the 2.5% interest rate serviceability buffer that applied up to October last year. In this scenario home prices could fall by around 30%.

On the upside several factors will help put a floor under prices and eventually drive a recovery. These include: government support programs (eg, home deposit schemes, “Help to Buy” schemes and NSW first home buyers swapping stamp duty for land tax); the tight rental market; & rapidly rising immigration. But for now, the property market will be dominated by higher rates. A pause in rate hikes on its own is unlikely to be enough to drive an upswing in prices as the capacity of buyers to pay will still be depressed. The last two major upswings in property prices that started in 2012 and 2019 required rate cuts before prices started to rise – see the purple ovals in the third chart in this note. Right now, we don’t anticipate rate cuts to start until late next year or early 2024.

Source: AMP Capital December 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Five medium term inflation pressures & implications for investors

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

IntroductionIt’s often said you don’t realise how good something is until it’s gone. This may apply to the low inflation environment that prevailed up to the pandemic. Apart from a few nasty interruptions this saw a downtrend in interest rates, mostly low unemployment, and an upwards trend

Read MoreDr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

It’s often said you don’t realise how good something is until it’s gone. This may apply to the low inflation environment that prevailed up to the pandemic. Apart from a few nasty interruptions this saw a downtrend in interest rates, mostly low unemployment, and an upwards trend in asset values (albeit it wasn’t so good for housing affordability). The explosion in inflation over the last year and the associated surge in interest rates and slump in investment markets makes it all seem like a distant memory.

The good news is that, as we noted in our last note (here), there is reason to believe the short term surge in inflation may be peaking (led by the US) & this, along with various other factors, may result in a better cyclical outlook for shares over the next 12 months. The bad news, as we have noted in various reports (see, eg, here), is that we have likely seen the bottom in the long-term decline in inflation from the early 1980s and inflation is likely to be higher over the medium term than pre-pandemic. This note takes a look at the five key structural factors driving this. (Two of these are a subset of global trends covered by my colleague (see here).)

1. Bigger govt, less economic rationalist policies

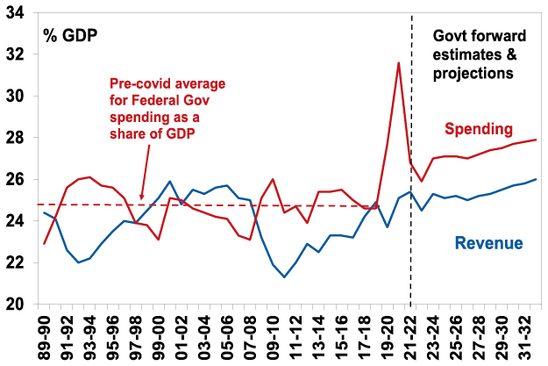

The reaction to the inflationary malaise of the 1970s was the economic rationalist policies of Margaret Thatcher, Ronald Reagan and Bob Hawke and Paul Keating in Australia. These focussed on boosting the ability of the economy to supply goods and services by: limiting government involvement in the economy through policies such as deregulation and privatisation; policies to boost competition; measures to boost incentives by lowering tax rates; and labour market reform to make labour markets more flexible. This all helped lower inflation. Now as a result of the problems highlighted by the GFC, rising inequality, stagnant wages, aging populations, climate concerns and a collective memory loss regarding the lessons of the past there is a backlash against economic rationalist policies and more support for government intervention in the economy. It’s evident in Australia, for example, with the rising trend in government spending and revenue as a share of the economy, widespread pressure to raise taxes, together with measures to return to multi-industry bargaining within the labour market. The risk is that greater government involvement in the economy leads to lower productivity growth which will hamper the supply side of the economy and add to inflationary pressure.

Federal Government spending and revenue

Source: Australian Treasury, AMP

2. The reversal of globalisation

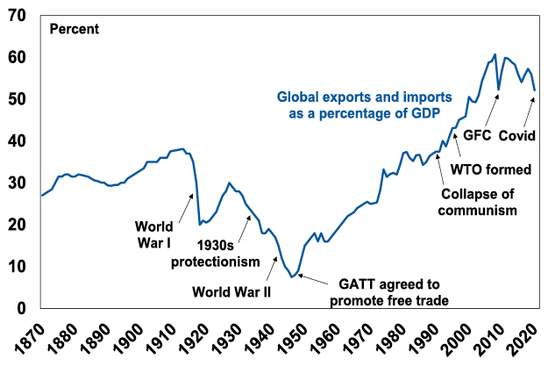

The post-World War Two period saw a huge surge in global trade and financial links between countries as more countries entered the global trading system and trade barriers collapsed. This saw a huge rise in global trade as a share of global GDP since the end of WW2 and the General Agreement on Tariffs and Trade (GATT). This was given a boost from the 1990s with the integration of China and Eastern block countries into global trade along with the formation of the World Trade Organization. This saw production allocated globally according to comparative advantage and the development of highly integrated global supply chains. The cost reductions and competition helped reduce inflation.

Globalisation through time

Source: World Bank, BCA, AMP

But the trend towards freer trade stalled in the 2000s, trade barriers are on the rise and trading blocks are being formed. The pandemic and rising geopolitical tensions are accelerating this reversal as countries seek to onshore production to reduce threats to supply chains spurred on by resurgent nationalist sentiment and a return to scepticism of free trade. The reversal of globalisation looks like it has a way to play out yet. Inevitably it will lead to higher costs and hence inflationary pressure.

3. Increasing defence spending

Over much of the last 60 years world military spending as a share of global GDP has been in decline. The most recent fall started in the 1980s and got a push along by the ending of the Cold War. This took pressure off metal prices (as military spending tends to be metal intensive) and it helped keep government spending down, which freed up resources for use by the private sector. Both of which were disinflationary.

World Military Expenditure (% of GDP)

Source: World Bank, SIPRI, AMP

Now military spending is on the rise again, spurred on by the Russian invasion of Ukraine & China tensions. Even Germany & Japan are boosting military spending, as is Australia. This means more demand for metals and more government spending which will add to inflationary pressure.

4. Climate change and decarbonisation

Ultimately the shift to sustainable energy could result in lower costs as energy from sources like wind and solar is cheaper than energy from most fossil fuels & still getting cheaper as the technology evolves. But we are a long way from that yet and climate change and the transition to net zero will likely add to costs & inflation in multiple ways via: increased extreme weather damage resulting in higher and more variable food and road transport costs; associated rebuilding costs & higher insurance premiums; costs associated with mitigation; increased demand for metals as economies retool for sustainability (eg an electric car uses 6 times more copper than a petrol car); increased energy costs as we are not seeing the usual supply enhancing investment response in fossil fuels to higher energy prices; and increased pollution regulation will add to costs like the anti-pollution equipment of the 1970s added to inflation at the time.

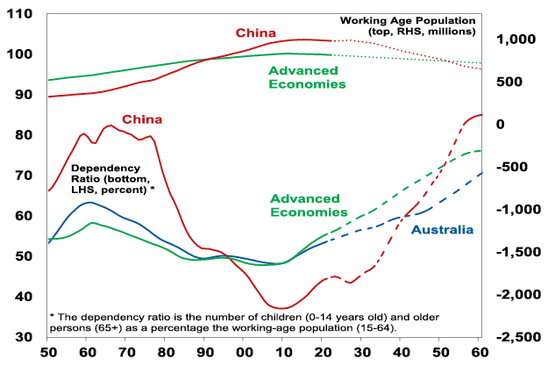

5. Less workers, more consumers

Demographic trends are changing in a number of key ways. Global population growth is slowing, while in advanced countries and China the working age population is now in the process of peaking and starting to decline (see the top portion of the next chart). And, as is well known, populations are aging, resulting in a rise in the ratio of children and older people to working aged people, ie the dependency ratio is rising (bottom portion of the next chart). Thanks to its high immigration program Australia is in a somewhat better position (with a still rising workforce and slower rising dependency ratio). But globally, the upshot is less workers (supply) & more consumers (demand) which will likely add to inflationary pressures. Similarly, “adverse for inflation” demographic trends are flowing from the entry to the workforce of inexperienced millennials and Gen Z as highly experienced baby boomers retire (which is bad for productivity) and the pandemic refocussing workers on quality-of-life making them more demanding in terms of pay and/or retiring early.

Dependency Ratio & Working Age Population

Source: UN, AMP

Implications for inflation

RBA Governor Lowe has referred to some of these structural forces as adding to inflation variability. But they are also likely to make economies more inflation prone as they imply more constrained supply & increased demand in some areas. For the technically minded this implies the supply curve shifting to the left and potentially being steeper and the demand curve (eg, for commodities) potentially shifting to the right. There is some offset with technological innovation still bearing down on prices, but the net effect will likely mean higher average inflation and possibly greater variability in it over time than pre-pandemic. The more inflation prone environment means central banks will have to work harder to keep inflation down around their 2-3% targets than pre-pandemic. Higher household debt levels in countries like Australia will aid in this as it makes monetary policy more potent than it was in the 1970s when household debt was low. It will probably still require higher & more variable interest rates than we saw pre-pandemic though.

Implications for investment returns

The collapse in inflation from the 1980s provided a tailwind for investment returns relative to what nominal growth and investment yields would normally indicate because it meant: lower interest rates; reduced economic volatility and uncertainty (and hence lower risk premiums); and a higher quality of company earnings. For growth assets it meant a valuation boost as shares traded on higher price to earnings multiples and real assets like property traded on lower income yields.

Higher inflation over the medium term than in the pre-pandemic period will remove this tailwind and threaten its reversal:

-

Higher interest rates will make cash and fixed interest relatively more attractive to investors.

-

Price to earnings ratios on shares will likely settle at lower levels and income yields on real assets at higher levels.

-

Higher mortgage rates will mean a lower capacity to borrow and hence pay for homes meaning more constrained home prices.

If inflation averages around central bank targets, which is our base case, returns will be constrained but still reasonable. If alternatively, inflation turns out much higher then returns risk being weak. Which makes it very important central banks are successful in keeping inflation down – it’s just that the structural backdrop means it will likely be harder going forward.

Source: AMP Capital November 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.